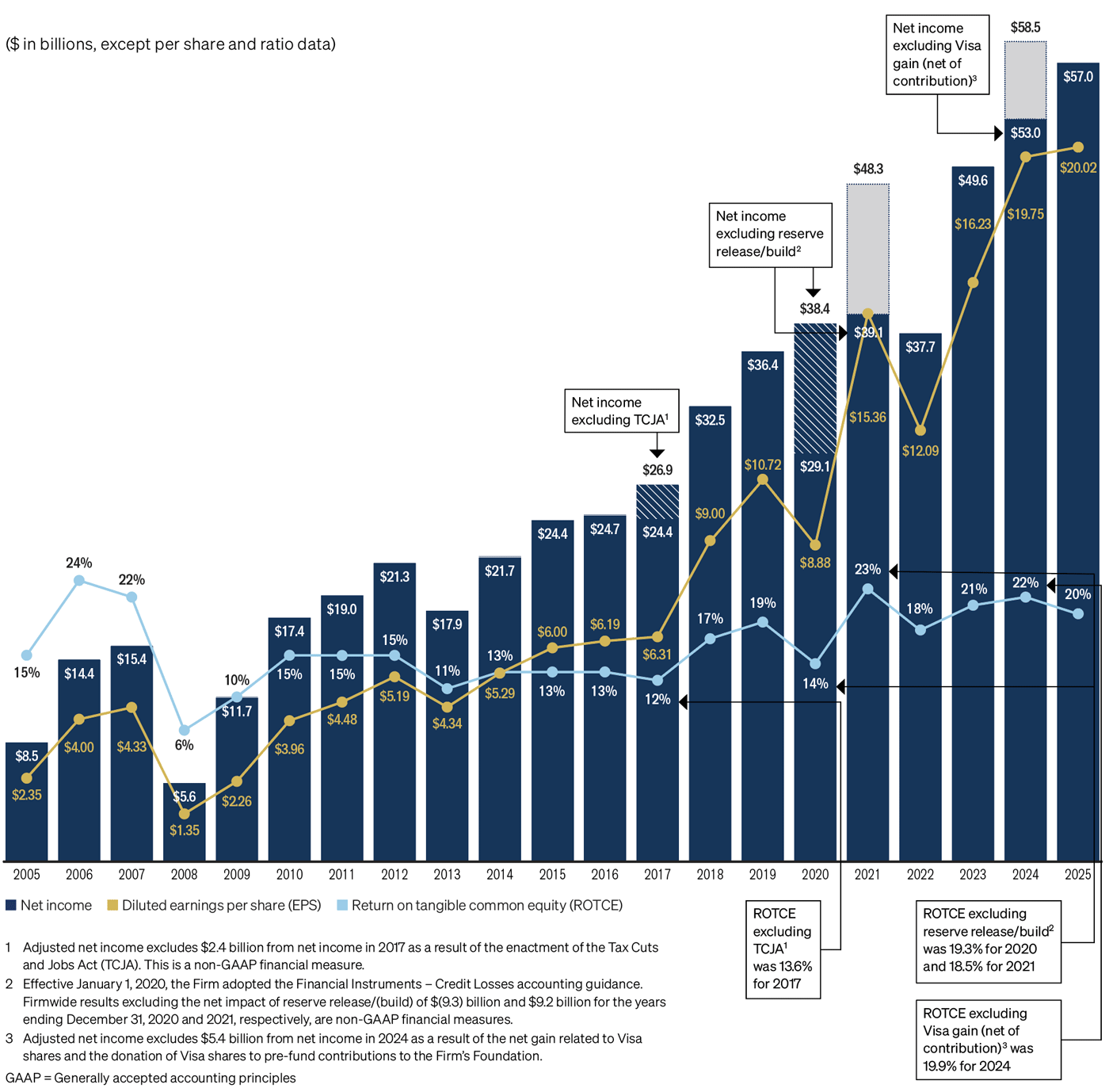

Earnings, Diluted Earnings per Share and Return on Tangible Common Equity 2005–2025

Creating thriving communities together

See how our clients and partners—from small business owners to workforce training leaders—work with JPMorganChase to drive meaningful impact and economic growth where they live and work.

Learn moreLatest news

Veteran’s Unconventional Path to Landing her Dream Job in Tech

U.S. Army Veteran Ashley Wigfall transitioned to a civilian role and charted her path to technologist through mentorship and skills training at the JPMorgan Chase tech hub in Plano, Texas.

Learn more

2025 ANNUAL REPORT

April 6, 2026

We are champions of banking’s essential role in a community — its potential for bringing people together, for enabling companies and individuals to attain their goals, and for being a source of strength in difficult times.

In 2026, America is celebrating its 250th anniversary. Also this year, we are celebrating the 227th anniversary of JPMorganChase, which was founded in April 1799. This is the perfect time to rededicate ourselves to the values that made this great nation of ours — freedom, liberty and opportunity — and to recognize that we all stand on our country’s shoulders.

The challenges we all face are significant. The list is long but at the top are the terrible ongoing war and violence in Ukraine, the current war in Iran and the broader hostilities in the Middle East, terrorist activity and growing geopolitical tensions, importantly with China. Our hearts go out to those whose lives are profoundly affected by these crises. We sincerely hope these global conflicts are properly resolved and that one day all of Europe and the Middle East will attain long-term stability and prosperity. Even in troubled times, we have confidence that America will do what it has always done — look to the values that have defined our singular nation and sustained our leadership of the free world.

Despite the unsettling landscape, the U.S. economy continues to be resilient, with consumers still earning and spending (though with some recent weakening) and businesses still healthy. It is important to note that our economy has been fueled by large amounts of government deficit spending and past stimulus and that increased expenditure on infrastructure remains a growing need. Now, because of the war in Iran, we additionally face the potential for significant ongoing oil and commodity price shocks, along with the reshaping of global supply chains, which may lead to stickier inflation and ultimately higher interest rates than markets currently expect. Continual trade negotiations exacerbate the tense geopolitical issues. And high asset prices, which certainly feel good in the short run, create additional risk if anything goes wrong. In Section III of this letter, I describe in greater detail how we are dealing with these risks.

JPMorganChase, a company that historically has worked across borders and boundaries, will do its part to ensure that the global economy is safe and secure, but we cannot confidently predict the outcome of current events, and our company is not immune to their ultimate effects. As we have for more than two centuries, we will continue to work through all of the complexities that confront us and continue to help our clients, including governments, always defending our values, even when challenged.

Remember the poem “If—” by Rudyard Kipling that begins “If you can keep your head when all about you are losing theirs”? We will stay true to this. We must deal with the world we have — and strive for the one we want.

Two things are absolutely foundational to our long-term success: The first is that we run a great company, and the second, which is maybe more important, is that the vitality of America domestically and the future of the free and democratic world are strong. In the first part of this letter, I talk about issues unique to JPMorganChase and how we are addressing them, including constantly surmounting complexity, bureaucracy and complacency. And in the last two sections, I focus on the perils before us, both nationally and internationally, that require urgent, effective solutions.

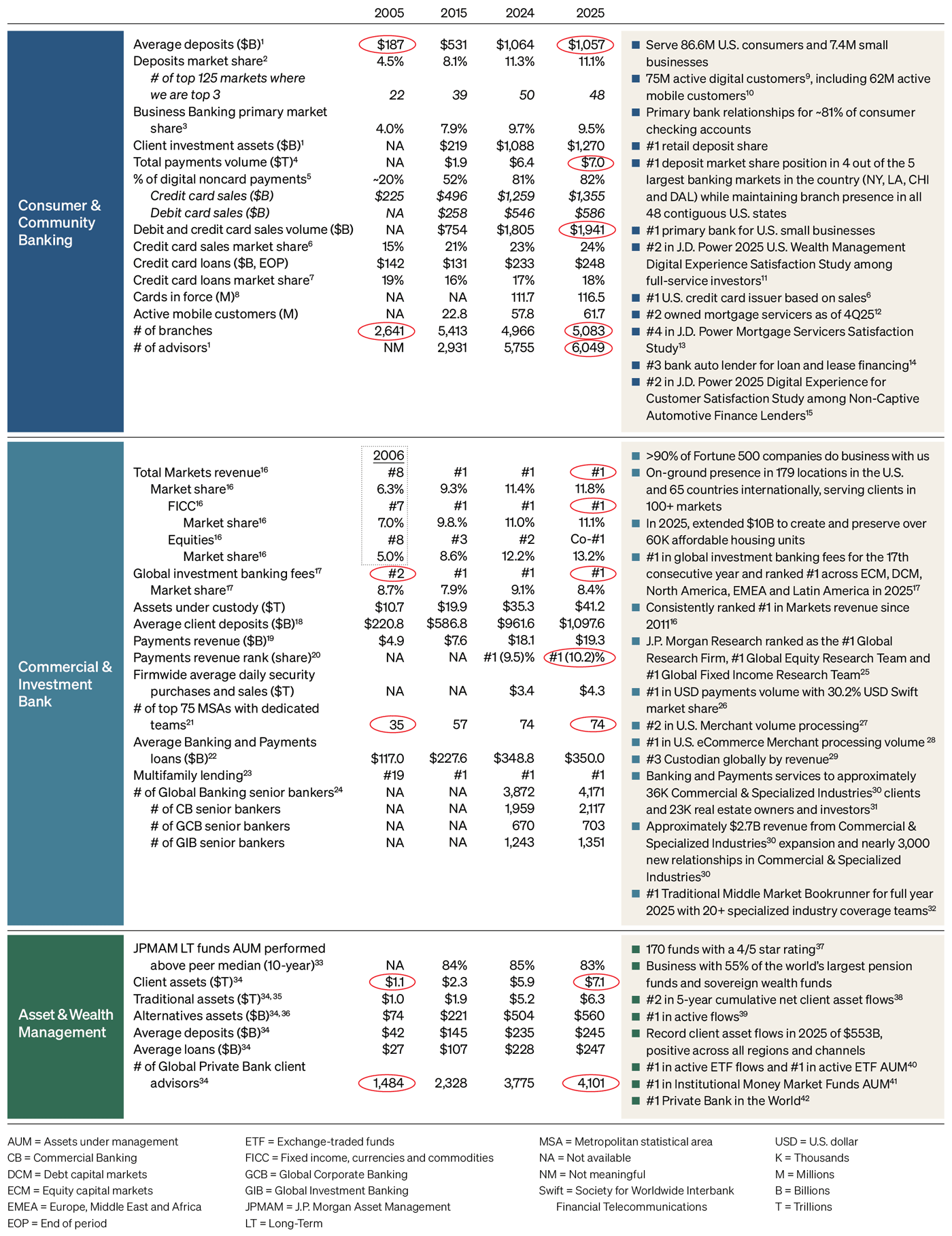

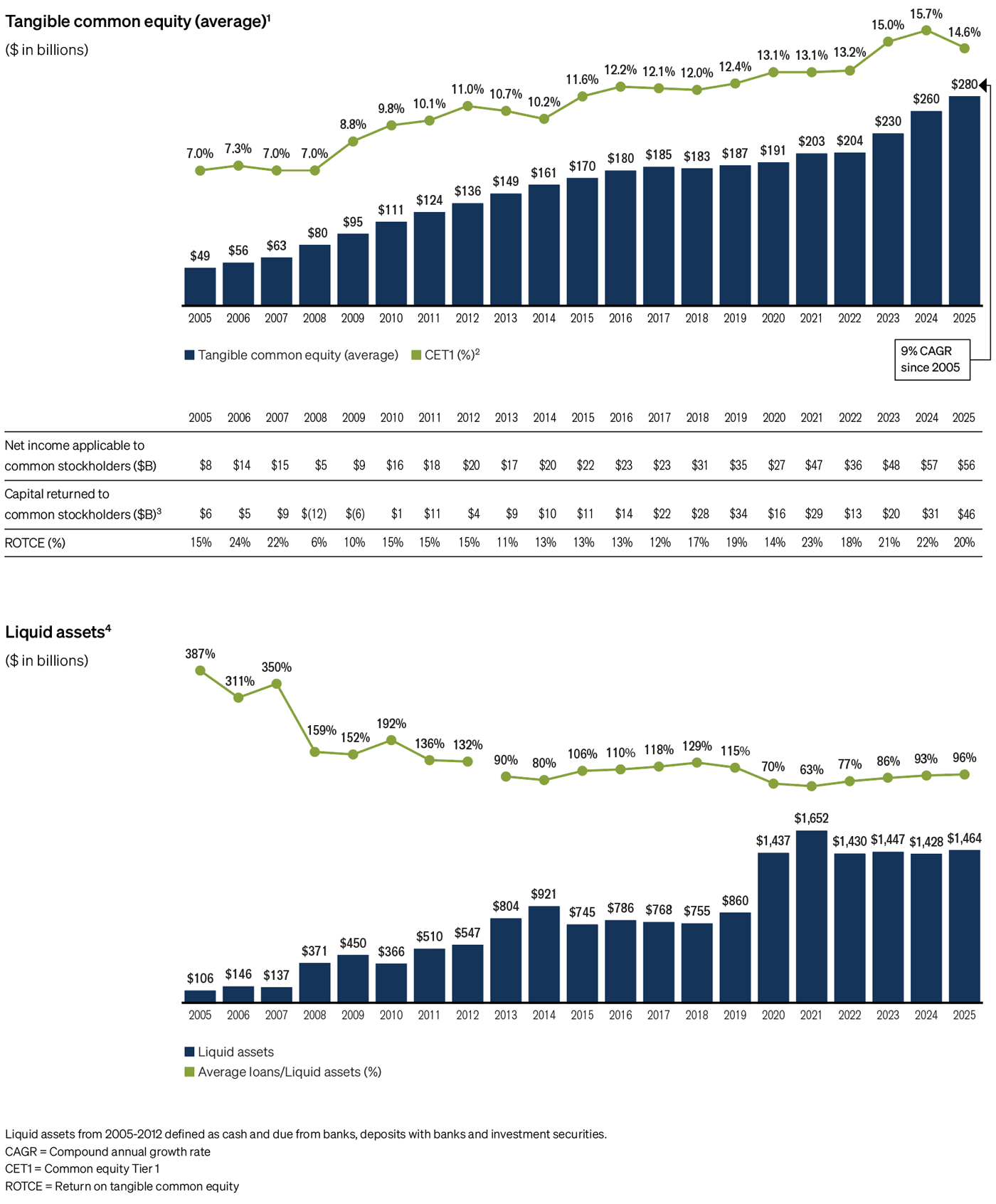

Throughout 2025, JPMorganChase demonstrated the power of its investment philosophy and guiding principles, as well as the value of being there for clients — as we always are — in both good times and bad times. The result was continued broad healthy growth across all our franchises, with the firm generating record revenue for the eighth consecutive year and setting numerous records in each of our lines of business. We earned revenue in 2025 of $185.6 billion1 and net income of $57.0 billion, with return on tangible common equity (ROTCE) of 20%, reflecting a strong underlying performance across all of our businesses.

We also increased our quarterly common dividend from $1.25 per share to $1.40 per share in the first quarter of 2025 — and again to $1.50 per share in the third quarter of 2025 — while continuing to reinforce our fortress balance sheet. We grew market share in several of our businesses and continued to make significant investments in products, people and technologies while exercising strict risk disciplines. We have achieved our decades-long consistency by adhering to our key principles and strategies (see the sidebar on our steadfast principles below), which allow us to drive good organic growth and promote proper management of our capital (including dividends and stock buybacks).

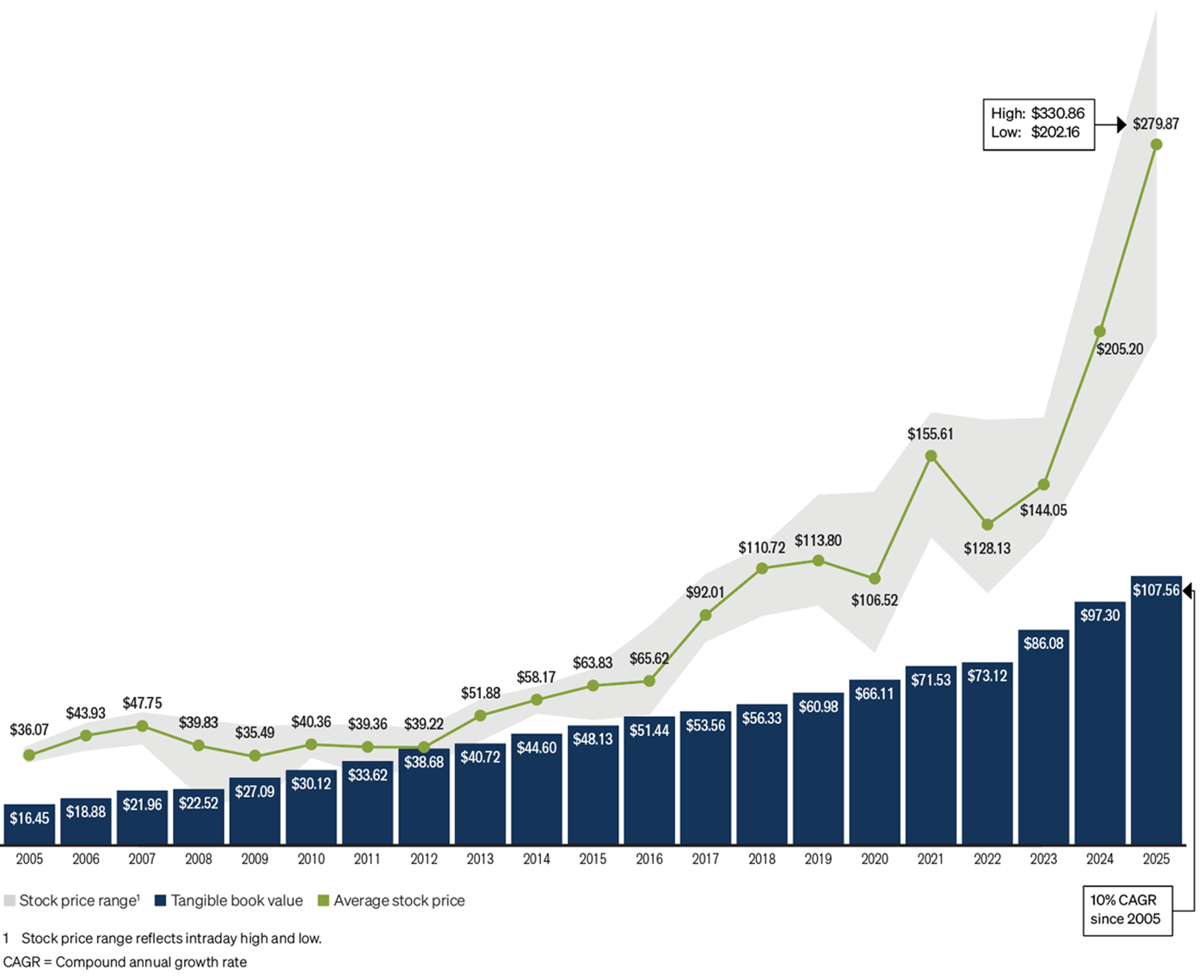

The charts below show our performance results and illustrate how we have grown our franchises, how we compare with our competitors and how we look at our fortress balance sheet. Please peruse them and the CEO and COO letters in this Annual Report, all of which provide specific details about our businesses and our plans for the future.

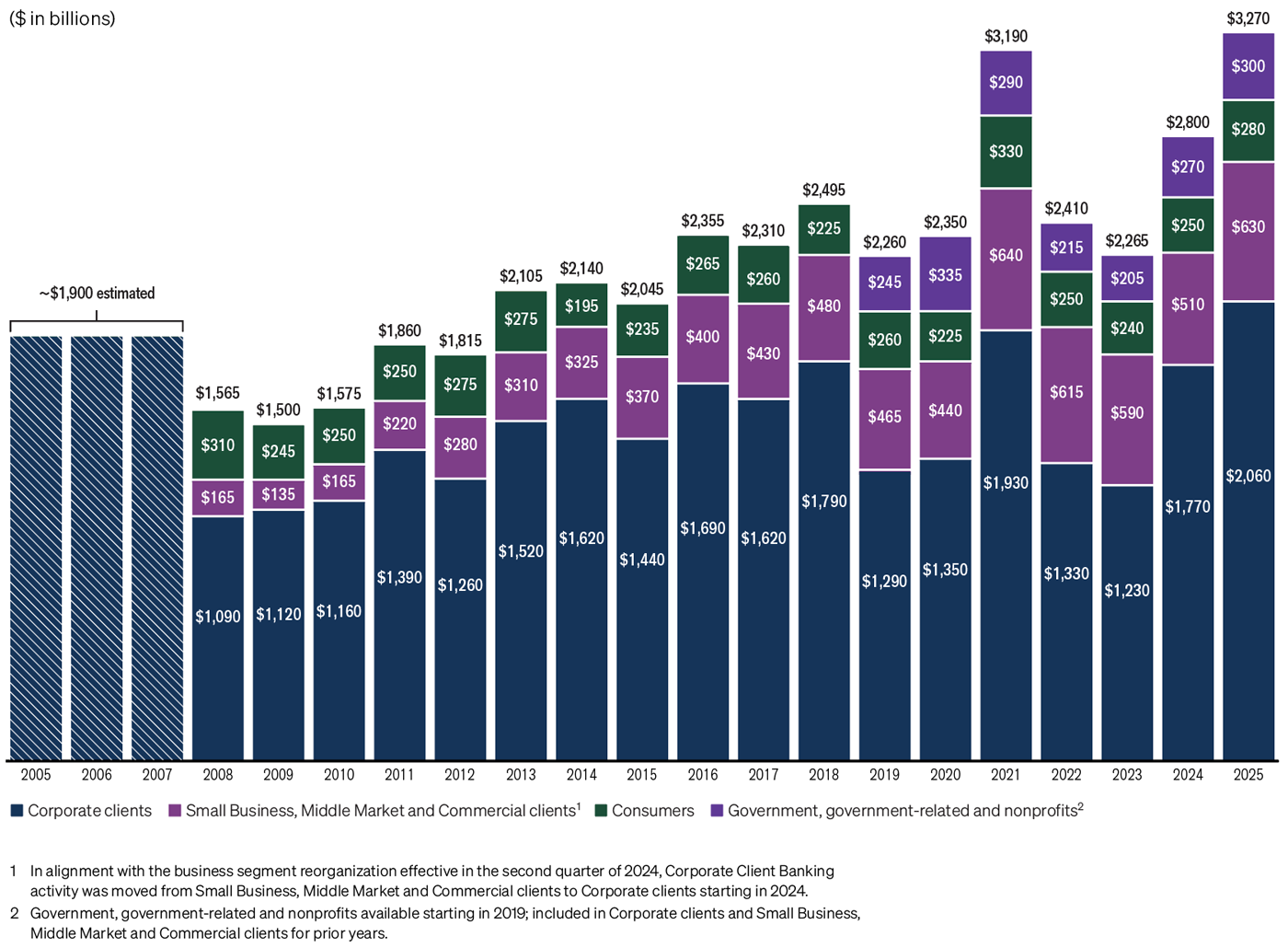

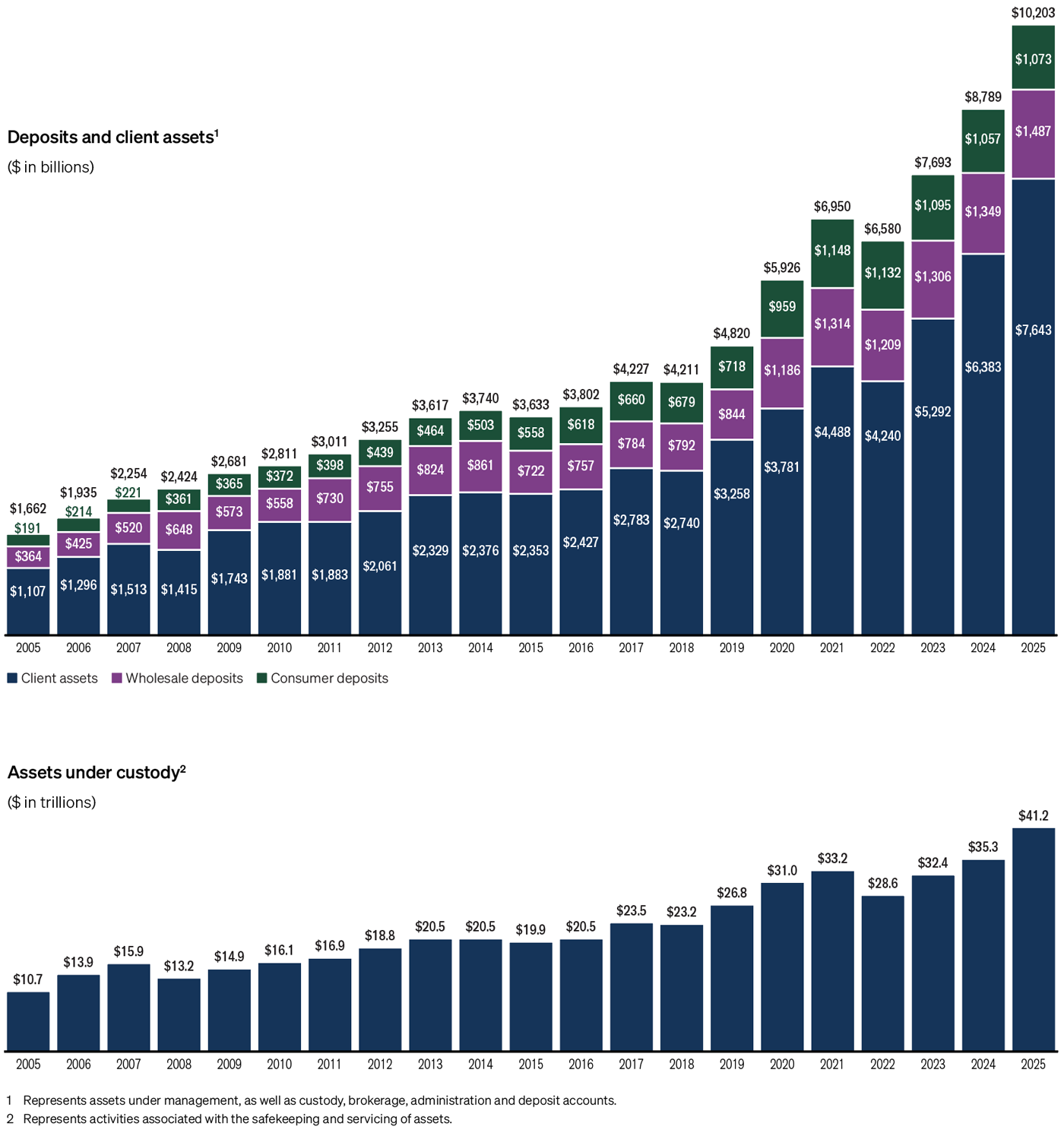

In 2025, we continued to play a forceful and essential role in advancing economic growth. In total, we extended credit and raised capital amounting to $3.3 trillion for our consumer and institutional clients around the world. On a daily basis, we move nearly $12 trillion in 120+ currencies and more than 160 countries, as well as safeguard over $41 trillion in assets. Bank deregulation will make it easier for financial institutions to support our growing economy, and, I believe, if properly done, it can actually make the banking system safer. More on this in Section I.

Amidst the extreme challenges of the last two decades, we have never stopped doing all the things we should be doing to serve our clients and our communities. As you know, we are champions of banking’s essential role in a community — its potential for bringing people together, for enabling companies and individuals to attain their goals, and for being a source of strength in difficult times. We remain as committed as ever to reaching out to all communities in an effort to create a stronger, more inclusive economy. We recently launched two ambitious initiatives, the Security and Resiliency Initiative (described in detail in Sections I and IV) and the American Dream Initiative (highlighted in Section I), both inspired by our resolve to offer our expertise to help address the needs of our country and what’s best for all Americans. We hope these commitments also demonstrate how business and government leaders can work together to solve seemingly intractable problems. These efforts are also commercial in nature — and they are no different from what most businesses large and small are trying to do in towns across America.

I often remind our employees that the work we do matters and has impact. United by our principles and purpose, we help people and institutions finance and achieve their aspirations, lifting up individuals, homeowners, small businesses, larger corporations, schools, hospitals, cities and countries in all regions of the world. I remain proud of our company’s resiliency and of what our hundreds of thousands of employees around the world have achieved, collectively and individually. We owe them a great debt of gratitude.

1. Represents managed revenue.

Looking back on the past two+ decades — starting from my time as Chairman and CEO of Bank One in 2000 — there is one common theme: our unwavering dedication to help clients, communities and countries throughout the world. Clearly our financial discipline, constant investment in innovation and ongoing development of our people have enabled us to achieve this consistency and commitment. In addition, across the firm, we uphold certain steadfast tenets that are worth repeating.

First, our work has very real human impact. While JPMorganChase stock is owned by large institutions, pension plans, mutual funds and directly by single investors, the ultimate beneficiaries, in almost all cases, are individuals in our communities. More than 100 million people in the United States own stocks; many, in one way or another, own JPMorganChase stock. Frequently, these shareholders are veterans, teachers, police officers, firefighters, healthcare workers, retirees, or those saving for a home, education or retirement. Often our employees also bank these shareholders, as well as their families and their companies. Our management team goes to work every day recognizing the enormous responsibility that we have to all of our shareholders.

Second, shareholder value can be built only if you maintain a healthy and vibrant company, which means doing a good job of taking care of your customers, employees and communities. Conversely, how can you have a healthy company if you neglect any of these stakeholders? As we have learned over the past few years, there are myriad ways an institution can demonstrate compassion for its employees and its communities while still strengthening shareholder value.

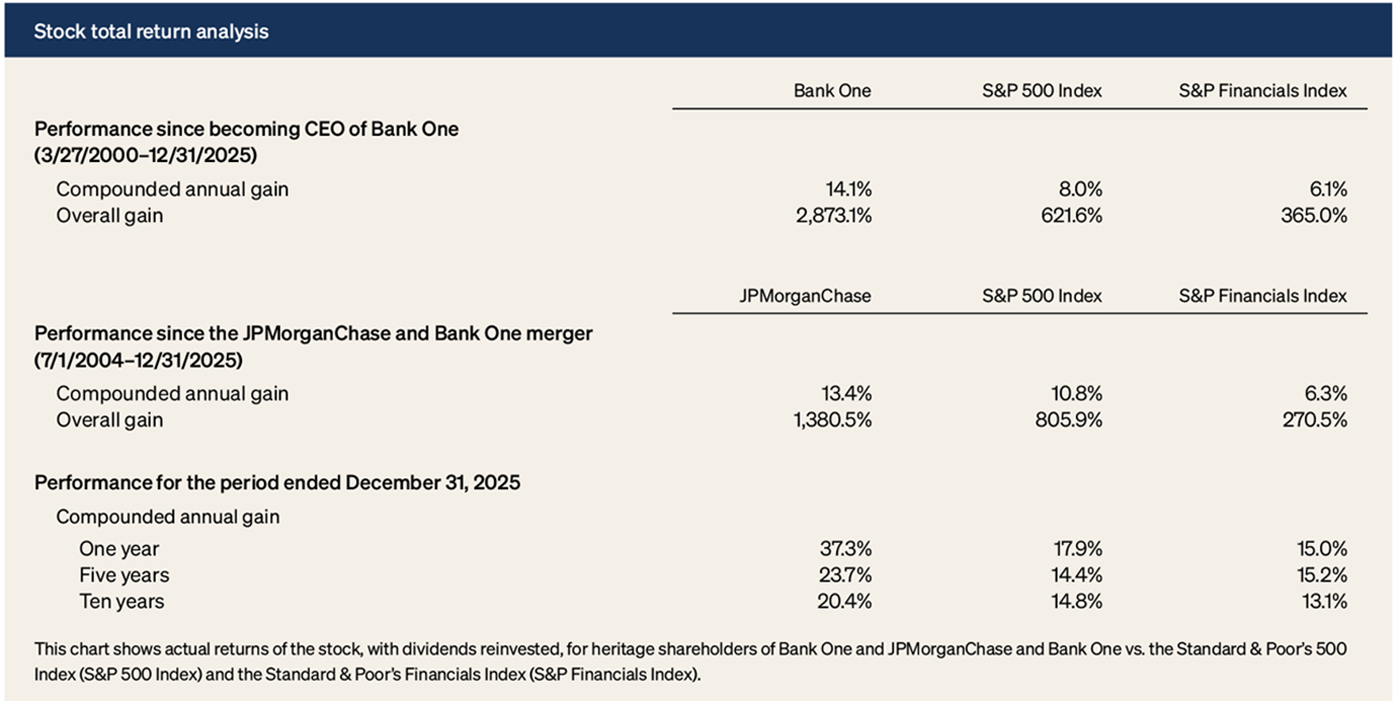

Third, while we don’t run the company worrying about the stock price in the short run, in the long run we consider our stock price a measure of our progress over time. This progress is a function of continual investments in our people, systems and products, in good and bad times, to build our capabilities. These important investments also drive our company’s future prospects and position it to grow and prosper for decades. Measured by stock performance, our progress is exceptional. For example, whether looking back 10 years or even further to 2004, when the JPMorganChase/Bank One merger took place, we have outperformed the Standard & Poor’s 500 Index and the Standard & Poor’s Financials Index.

Fourth, we are united behind basic principles and strategies (you can see the principles for How We Do Business on our website and our Purpose statement in my letter from 2022) that have helped build this company and made it thrive. These allow us to maintain a fortress balance sheet, constantly invest and nurture talent, fully satisfy regulators, continually improve risk, governance and controls, and serve customers and clients while lifting up communities worldwide. This philosophy is embedded in our company culture and influences nearly every role in the firm.

Fifth, we strive to build enduring businesses, which rely on and benefit from one another, but we are not a conglomerate. This structure helps generate our superior returns. Nonetheless, despite our best efforts, the walls that protect this company are not particularly high — and we face extraordinary competition. I have written about this reality extensively in the past and cover it again in this letter. We recognize our strengths and vulnerabilities, and we play our hand as best we can.

Sixth, we must be a source of strength, particularly in tough times, for our clients and the countries in which we operate. We must take seriously our role as one of the guardians of the world’s financial systems.

Seventh, we operate with a very important silent partner — the U.S. government — noting, as my friend Warren Buffett points out, that his company’s success is predicated upon the extraordinary conditions our country creates. He is right to have said to his shareholders that when they see the American flag, they all should say thank you. We should, too. JPMorganChase is a healthy and thriving company, and we always want to give back and pay our fair share. We do pay our fair share — and we want it to be spent well and have the greatest impact. To give you an idea of where our taxes and fees go: In the last 10 years, we paid more than $44 billion in federal, state and local taxes in the United States and over $30 billion in taxes outside of the United States. Additionally, we paid the Federal Deposit Insurance Corporation (FDIC) over $13 billion so that it has the resources to cover failures in the American banking sector. Our partner — the federal government — also imposes significant regulations upon us, and it is imperative that we meet all legal and regulatory requirements imposed on our company.

Eighth and finally, we know the foundation of our success rests with our people. They are the front line, both individually and as teams, serving our customers and communities, building the technology, making the strategic decisions, managing the risks, determining our investments and driving innovation. However you view the world — its complexities, risks and opportunities — a company’s prosperity requires a great team of people with guts, brains, integrity, enormous capabilities and high standards of professional excellence to ensure its ongoing success.

Within this letter, I discuss the following:

I. Specific Issues Facing Our Company

III. Managing in a Time of Increasing and Complex Risks

IV. Critical Issues Facing America and the World

The last five years have been a period of significant growth for us — as evidence, we added more than 60,000 people to our workforce, we opened over 900 branches across the United States, and we launched multiple new products and services. In the following section and in the letter by our Chief Operating Officer, we share various ways we seek to keep our company healthy, including specific efforts designed to maintain our grit, our leading position and our efficiency. We are keenly aware that our competition around the world is always gaining.

Our shareholders should recognize, as we do, that our company faces strengthened traditional competitors, including large banks in the United States, regional banks, strong international banks, large and successful money managers, and strong investment banks.

As I’ve detailed in previous letters, our rivals increasingly include a large and growing set of nontraditional and fintech competitors globally in areas such as payments, digital banking and investing, and global market making. I’m not going to mention all their names, but you can imagine that we study and track over a hundred of them.

While we have been able to grow, many but not all of the new players have been quite successful and continue to raise both money and their ambitions. In addition, a whole new set of competitors is emerging based on blockchain, which includes stablecoins, smart contracts and other forms of tokenization.

Our ongoing success will be based on our ability to wisely invest and move very quickly and nimbly, especially around product design and rollout, including incorporating artificial intelligence (AI) in everything we do. While much of what we do will remain the same — serving people and businesses needing to hold money, move money, invest money, raise money and manage their investments — new competitors and new technologies may change the fundamental nature of how all this is done.

While the competition is fierce, we do believe in most cases we will be able to sustain our top-ranking performance. In the section on management learnings, I discuss what we need to do as a management team to ensure our ongoing success.

Some of our growth opportunities are basic and exist in every detailed segment level. In Consumer & Community Banking (CCB), we continue to add, train and enable bankers and advisors to serve more clients. We’re expanding our branch network to capture share in underpenetrated markets, including more rural markets across the country. And we’re investing in marketing and product refreshes to drive card account growth, as well as scaling natural adjacencies in wealth management and commerce to address more of our customers’ needs. In the Commercial & Investment Bank (CIB), we’re expanding to more countries and regions, securing growth in private markets and building upon our capabilities in global payments and digital assets. And in Asset & Wealth Management (AWM), we are continuing to invest in our active management capabilities, enhancing our alternatives and exchange-traded fund platforms, expanding our international footprint and adding Global Private Bank advisors.

You can read about these plans more specifically in the CEO letters.

We need to do a better job of utilizing our data to help the customer. We must develop products quicker and always look at the adjacencies that can make a customer’s life easier. We need to roll out our own blockchain technology and continually focus on what our customers want in a very detailed way.

Size can often be a tremendous business disadvantage because it frequently comes with the baggage of complexity, bureaucracy and complacency. It can slow down decision making, generate arrogance and cloud the essential focus on seeing the world through the customer’s eyes. Being a company of sizable magnitude makes it easier to ignore new competitors since they often start small in one product but move rapidly to expand. The most successful examples of these are Block, Citadel Securities, Revolut and Stripe.

However, scale, capital and capabilities are going to matter more with the enormous investments that need to be made in global infrastructure — technology, new supply chains, AI and enhancements that meet government needs. In some of these cases, our size, capital and capabilities can be a relatively good competitive advantage.

They are outlined as follows:

Our Security and Resiliency Initiative (SRI) is already well underway and, in fact, will help us grow. It is explained in greater detail in the last section of this letter but, broadly speaking, describes our deployment of capital and expertise to support industries critical to the military and economic security of the United States and its partners. We have a lot to catch up on and not much time.

I continue to believe the American Dream is alive, but it’s slipping out of reach for too many people — and it’s now affecting generations of families. This slows economic growth, hurts communities and prevents many people from getting ahead. Further, it deeply damages Americans’ faith and confidence in their country.

That is why JPMorganChase recently announced the American Dream Initiative (ADI) — a firmwide multi-year effort to expand opportunity to millions of Americans through targeted investments in local communities across the United States. It builds on our firm’s years of experience of investing in local solutions that work.

We will focus on six areas where we have deep expertise that helps drive meaningful impact:

We are starting by supporting 10 million small businesses — up from 7 million served today — over the next several years. As the nation’s leading small business bank, we intend to scale support for small businesses by deploying increased capital and providing more financial coaching, advice, training and tools.

We’re also taking the American Dream to the local level — and our presence in Detroit proves that point. When we went there in 2014, we looked at what the city needed and how investments from our firm could make a meaningful difference, targeting areas where we could make the greatest impact. We must continue these efforts, learning from successes like Detroit. That city spawned many initiatives at our company (think our Service Corps and AdvancingCities), but most important, it showed how proper collaboration between business and government can help to tackle some of our biggest problems.

Now we want to replicate and scale what works. ADI will be nationwide with a particular focus on amplifying impactful work already happening in certain markets, such as Alabama, Atlanta, Los Angeles, Philadelphia and San Francisco. Please read the sidebar below, which shows how we’re going deep and local in Alabama.

We need to support policies that create jobs, foster upward mobility and ensure everyone has a fair shot. This could go a long way to solving affordability challenges, too. Jobs create dignity and self-worth — and attaining that first rung almost always leads to the second, which, in turn, fosters many positive social outcomes.

The dream of enjoying freedom, taking care of your family, experiencing good health and making the most of opportunity is not just an American aspiration, it’s a global one.

For over 50 years, JPMorganChase has helped drive economic and job growth, support businesses of all sizes and put the American Dream within reach for more Alabamians. It’s clear that Alabama’s future is bright, and we are excited for what’s next.

We’ve been working hand in hand with local governments, businesses and community partners to understand how we can best use JPMorganChase’s full range of resources to complement their efforts. I was honored to meet with many of these leaders during our bus tour through Alabama last summer. The state’s expansive economic growth has opened up immense opportunity for the residents and businesses of Alabama.

We proudly serve more than 590,000 Consumer Banking customers, helping them buy homes and save for the future. We bank over 29,000 small businesses statewide, as well as key institutions like Auburn University, the University of Alabama, Children’s Hospital of Alabama and Infirmary Health System, among others. We also finance critical infrastructure, including a recent $730 million Alabama Highway Authority bond for the West Alabama Corridor project.

This year we are deepening our efforts in Alabama as part of our recently announced American Dream Initiative. This includes new programs and ideas that you’ll hear more about in the coming weeks and months, such as:

Many of these efforts align with our Security and Resiliency Initiative, a $1.5 trillion, 10-year plan to facilitate, finance and invest in industries critical to national economic security and resiliency. We expect this to benefit companies, workers and communities in Alabama, a leader in advanced manufacturing, aerospace and defense.

Small and midsized businesses are the backbone of the state’s economy — the former alone employ nearly half of Alabama’s private sector workers. JPMorganChase will continue to help local entrepreneurs and businesses, like Astrion, headquartered in Huntsville, at every stage of their growth secure access to capital, supply chain opportunities and other essential resources to thrive.

This includes a recent $2 million philanthropic investment to launch the Alabama Capital Access Collaborative aimed to help small businesses gain improved access to capital and achieve greater efficiencies, as well as assist local community development finance institutions and other community lenders in improving their lending, investing and operational capacity.

Moving forward, we’re helping local small businesses overcome barriers to serving as suppliers in Alabama’s growing aerospace, defense and government industries by providing mentorship, capital and upskilling to compete for supply chain contracts. It can be costly and difficult for smaller companies to meet the requirements, including cyber readiness.

Additionally, we’re expanding our team of senior business consultants in branches across Alabama and providing more coaching and expert guidance on business planning, financial management and marketing.

A prosperous job market is the foundation of a strong economy — and in Alabama, demand is high for skilled workers, especially those who can perform technical work in the industries that are vital for America’s security and local economic growth.

With our support, the nonprofit Alabama Possible is working with community colleges to expand eight career advancement programs for adult learners in aviation, steel and aerospace. They’re also partnering with Alabama Power to support two accelerated training programs for HVAC technicians and utility line workers.

As we do more in Alabama, we intend to partner with additional community colleges and universities, business leaders, and groups that serve communities large and small to better connect local workers and employers. This includes expanding access to skills and job opportunities for veterans and strengthening apprenticeship pathways.

We’re working to help more Alabamians save money, build credit and achieve their financial dreams.

We are opening new branches in Decatur, Foley and Trussville this year as part of our plan to triple the number of Chase branches to 35 by 2030. We will also open our first Community Center in the state, which is designed with extra space for community events, financial health workshops, skills training and small business pop-ups. This effort will create more than 170 new jobs and help over 50% of the state’s citizens reside within an accessible drive of a Chase branch.

Through Chase Money Skills, Chase Secure BankingSM and Chase First BankingSM, we’re also helping people access digital financial tools and affordable banking products. Through our Birmingham-based Community Manager, we’re offering additional financial education and expanding our partnerships with community organizations and colleges. These collective efforts help with ways to boost credit scores and put residents on a pathway to homeownership.

By doing more in Alabama, we’re not just investing in the state’s economic future — we’re helping to secure America’s long-term economic resilience and security, with Alabama’s people and industries leading the way.

Our footprint includes:

Serving our clients and customers

Serving local institutions

Serving the local economy and communities

We are an extremely trusted partner in a world of growing distrust, particularly in the spheres of social media, commerce and use of data and where these intersect. There are a lot of risks associated with the misuse of customer data and commerce, which is likely to get far worse with AI and agentic commerce. We think there are large opportunities for us to act on behalf of our customers and in the way they want — as a truly trusted partner. We are continually improving our already strong capabilities to combat scams and fraud. We expect to roll out some products over the next two years that will build on what we already offer, particularly around control of personal data, safe commerce and customer-friendly algorithms. We also believe that some of our identity and fraud prevention capabilities can be extended to more third parties.

We have continued to grow our Wealth Management business through our branch bank model, J.P. Morgan advisors and Self-Directed Investing. In total, client investment assets in this area rose 17% in 2025 to $1.3 trillion. In 2026, we intend to make it much easier for clients to automatically move money from their regular checking account to higher-yielding brokerage products and vice versa so they can maximize yield while managing day-to-day cash flow. It won’t require multiple steps to trade, clear and transfer cash between accounts — our Smart Cash capability will do it for them. Eventually, AI will allow clients to predict cash flow needs and anticipate upcoming bills, doing their budgeting for them.

In 2026, we have also rolled out what we believe is best-in-class retail trade execution — basically giving consumers access to the same execution capability that the largest, most sophisticated investors in the world enjoy, which saves them money. We believe this is better than the execution provided when a broker is paid for order flow.

With clients facing unprecedented change, uncertainty and opportunity, we recognize that the traditional role of a banker is changing. In navigating complex challenges, clients are often seeking guidance far beyond typical financial advice. We’re commonly asked, “How does JPMorganChase approach this? How are you preparing for that? How do you protect the firm? How do you ensure operational resiliency?”

Special Advisory Services allows us to formally connect clients with our in-house experts leading critical areas such as AI, cybersecurity, digital assets, geopolitics, government affairs, real estate, risk, strategy, supply chain and talent management. This means our clients can draw on the same expertise and insights that guide our own firm through today’s most complex challenges.

Whether a client is preparing for a major IPO, planning a transformational deal or looking to grow their business with us as their primary bank, our commitment is to be there every step of the way. Sharing insights and best practices with them across so many aspects of their company can help them run a better business. It’s also one more way we can demonstrate our dedication to the client, understanding their challenges and strengthening our value as their partner for years to come.

We used to offer these services on an ad hoc basis, often by request. Now we intend to extend these extraordinary services further to companies that have a long-term relationship with us; i.e., we are one of their lead banks and have trusted relationships with their C-suite and board members.

Our excess capital, making many assumptions around regulatory reform, is approximately $40 billion. This $40 billion is effectively earning a 4% after-tax return. We now believe that over time we can deploy it at excellent returns. We will do this with our normal careful building of important customer relationships, which also means that it may take several years or so to deploy this capital.

In the meantime, we continue to pay healthy and increasing dividends. And we also continue to buy back enough stock so as not to increase total excess capital, though we have a number of options on how to deploy our capital and are clear-eyed that many asset prices, including bank stocks, are fully valued. We always prefer to deploy capital, if possible, and when we do that through share repurchases, we want it at prices that enhance the value for our ongoing shareholders.

Some of our excess capital is effectively deployed when we build new branches or hire new bankers, even though it is treated as an expense. We believe that the initiatives listed above and outlined in the CEO letters are effective uses of our deployable capital.

A properly regulated banking system helps reduce risk to the financial system, protect customers, and maximize productive use of capital and lending. The Dodd-Frank Wall Street Reform and Consumer Protection Act and some of the rules that followed that legislation accomplished some good things. At the same time, they also created a fragmented, slow-moving system with expensive, overlapping and excessive rules and regulations — some of which made the financial system weaker and reduced productive lending. Those regulations also created many rules and requirements that had nothing to do with safety and soundness, and in fact often took the regulators’ eyes off the real risk. The real risks almost always end up being credit, liquidity, interest rate or operational risk.

Many of the financial rules that were put in place did not originate from a clear idea about what they should be or what they should accomplish, which led to unintended consequences. Additionally, rules were often inconsistent from regulating body to regulating body — and many regulators were independently involved in so many regulations that they lacked an ability to make rapid or coordinated changes as needed. Of course, this was also very difficult for them. I am going to talk further about some of the negative consequences of bad bank regulations, but I also hope to provide some real solutions.

One other flaw of the banking regulations is that they were legislated in a way that made them open to completely different interpretations depending on your political point of view. As agency leadership changes, this has the effect of creating ping-pong regulations. It would be very helpful if legislators wrote more clearly crafted regulations across the board that minimized the risk of dramatically different political interpretations.

Not all bank regulations are all good or all bad — we should just try to get it right. I have a few suggestions.

One of the huge risks for a bank has always been a “run on the bank,” which occurs when people think that their uninsured deposits are at risk. The FDIC only covers insured deposits, and the run risk is driven by uninsured deposits, particularly nonoperating uninsured deposits. In recent bank failures, regulators have had to invoke the systemic risk exception (SRE) to protect uninsured deposits at the point of failure. That is a problem — no one should want this as an emergency mechanism. It creates moral hazard, and the process to invoke the SRE is chaotic and involves multiple agencies, including approval by the Treasury Secretary in consultation with the President. Bank runs can happen quickly, and relying on that type of action to avoid contagion is simply not a good idea. Here are some ideas that I believe would not only significantly reduce the chances that the SRE would need to be invoked but would also make the system safer and avoid moral hazard.

While it was good to see that the recent proposals for the Basel 3 Endgame (B3E) and GSIB attempted to reduce the increase in required capital from the 2023 proposals, there are still some aspects that are frankly nonsensical.

The GSIB surcharge is still broken. The original Basel rule, known as Method 1, was a grab bag of overlapping metrics — many of which had nothing to do with risk or resolvability — that solved for a number that international regulators thought was right. Then the United States decided that wasn't high enough and created Method 2, which basically was double Method 1. In the meantime, banks, including JPMorganChase, have made enormous progress addressing resolvability concerns while remaining profitable and becoming more resilient. Due to its methodological flaws, the bulk of the increase of our Method 2 surcharge has been driven by growth in the overall economy. Under the GSIB re-proposal, our surcharge would only decrease very modestly, to about 5.0%. This is absurd when we compare it with our 2015 Method 2 surcharge of 3.5%, and even more absurd when compared with our Method 1 surcharge of 2.5%, which has been flat versus inception.

A properly designed framework should reward the resilience and strength of our diverse income streams and strong risk management. With a surcharge of approximately 5.0%, JPMorganChase will have to hold as much as 50% more capital across the vast majority of loans to U.S. consumers and businesses when compared with a large non-GSIB bank for the same set of loans. While we can accept that some level of surcharge is appropriate, given our position in the market, the proposed level just seems to punish our success, our strength, our consistency and our balanced business model. Frankly, it’s not right, and it's un-American.

As I mentioned earlier, there are numerous flaws in the operational risk framework. Since the current proposal still retains this operational risk and hasn’t addressed all the duplication and flaws, we could show you some additional capital metrics that are a fairer representation of the strength of our balance sheet.

We support a timely finalization of the B3E and GSIB re-proposals: Everyone wants to move on, and there are new important areas that require focus, like liquidity regulation. But, unfortunately, the latest proposals are still very flawed in a few specific areas, so we will be pointing that out in our comment letters.

The importance of AI is real — and while I hesitate to use the word transformational — it is. The pace of adoption will likely be far faster than prior technological transformations, like electricity or the internet. Those took decades to roll out, but this implementation looks likely to accelerate over the next few years. Our Chief Operating Officer describes our efforts in more detail, but I want to make some key points here.

One last but important point: We have focused on some of the “known and predictable” and some of the “known unknown” events. But huge technological shifts like AI always have second- and third-order effects as well that can deeply impact society. Some of these are, for example, cars bringing about the development of suburbs and shopping malls; agriculture enabling cities; and the original internet (invented back in 1969) leading to mobile phones, apps and social media. We should be monitoring for this kind of transformation, too.

No matter who you are, you need to deal with reality and the truth. The truth is that while New York City has much going for it, particularly for financial companies (because of extraordinary local talent), it also has the highest city and state corporate taxes and the highest individual income and state taxes. People often make this a moral or loyalty issue, but it is not. Companies need to remain competitive in this very tough, fast-moving world. And higher taxes mean lower returns on capital and less competitiveness by their nature.

Additionally, individuals vote with their feet — you can already see a fairly large exodus of people and jobs out of some states with high taxes and high expenses (often due to high taxes and regulatory burdens). Sometimes you see companies leaving states, but migration also shows up in shifts of employees out of certain states. For example, while New York City is still our company’s global headquarters, we have shrunk our headcount in the city, from 30,000 a decade ago to 24,000 today, and increased our headcount in Texas, from 26,000 in 2015 to 32,000 today. This trend will likely continue.

Sometimes this can be a disaster for a city. I am reminded that in the 1970s, nearly half of the 125 Fortune 500 companies based in New York City left. While mergers accounted for some departures, the price of doing business in New York City accounted for most: cost of taxes, office rents, labor and so on. No city — or company or country — has a divine right to success.

We always enjoy every year musing about management lessons learned — and sometimes relearned. Sometimes we also discover that we need to change how we function because the world (technology, competitors, products, among other factors) has changed.

The real competitive battles are fought at the detailed segment level: It’s not just investment banking or the investment banking healthcare sector; it’s having the right team to win in healthcare pharma or medical devices. It’s not just credit card or even affluent brands; it’s the Chase Sapphire® card. It’s not small business clients in branches; it’s restaurateurs or law firms. It’s not digital payments; it’s 24/7 digital payments with automatic currency conversions. It’s hundreds of small teams (including technology, AI, marketing, subject matter experts and others) attacking specific problems. The teams needed to tackle these challenges should be small and authorized with the decision-making ability to move and act like Navy SEALs or the Army’s Delta Force. Finally, they need to be dedicated to the task at hand. Very often when a management team wants to accomplish something new, like create a digital account opening process that cuts across virtually every area, everyone on the team says, “We’ll get it done,” meaning they will add it to the long list of tasks already on their plate. But when efforts are 1% of a lot of people’s jobs, it will never get done. You need a team 100% dedicated to the mission — and everyone else supports them.

Success requires speed, agility and relentless execution. This is trench warfare; it’s about fighting for every inch, moving quickly and getting things done. Growth comes from out-working and out-innovating the competition, deploying our resources strategically and fine-tuning our initiatives to maximize impact.

We need to keep everything in motion, break down bureaucracy, and leverage our trusted brand and technological edge to win in every market where opportunity exists. I do believe that we have everything in motion for continuous progress.

While there is an unbelievable need for speed, these teams can’t all build their own systems. They need to rely on a common language, common tools and interoperability. Therefore, certain platforms (e.g., for data, AI, coding, financial and CRM systems) need to be companywide and easily deployed, which may mean they are necessarily large. Before they are deployed, it may require consensus that they are the best platform to use. This makes them reusable and highly efficient. The trick is to have great platforms without creating bureaucracy and to build great teams for speed.

It has been an immense pleasure and honor running this company. It has also been an extraordinary amount of hard work, long days and lots of travel. And I have often wondered if all of that effort was worthwhile. I have seen management teams that don’t work as hard or travel as much and still run a successful company. And I have seen companies that have multiple cultures and still seem to get by — at least in the short run. But I do not believe this company, with its complexity and extraordinary risk and global reach, could have survived or thrived that way. When I look back, I do believe the exceptional effort that we all made really made a huge difference.

Given the breadth of our company, these efforts take many forms. In addition to constant business reviews, management meetings, workout sessions, deep dives, client and employee lunches, and leadership offsites, our commitments are considerable, a sampling of which may help our shareholders better understand how we maintain our culture. Here are a few examples from the past 10 years:

This hard work is also fun as we celebrate our successes, and it is extremely informative as we learn from employees and customers about what we could do better. These extensive efforts and travel drive continuous improvement and inform how we educate our people to treat one another and our clients and deal with problems. One last note: Wherever I go, I get to observe our employees around the world getting to know our people in other parts of the firm and seamlessly collaborate with one another for the benefit of JPMorganChase and our clients. It’s gratifying to see this exceptional company in action.

One of the most rewarding parts of the bus trip for us is riding alongside some of our front-line employees — our bankers and advisors. Their perspective and advice on how we can do a better job are invaluable. And, boy, do we get a lot of advice — over the years, there have been hundreds of specific recommendations, which we implement as appropriate.

We want to make this drive toward continuous improvement a part of the fiber of every person at our firm.

Recently, I was blown away by the presentations of several of our executives (at a senior leaders’ meeting) and by the level of collaboration across every segment — consumer, private bank, investment bank, commercial bank and others. There’s a sense of momentum: I feel like we’ve got everything in motion and that we’re attacking our problems in multiple ways. If the senior leaders ever feel we’re too bureaucratic or slow, they speak up. Our challenge to them is: “Don’t wait. Get stuff done; get it fixed.” We need to make it an “always-on” process of streamlining and bureaucracy-busting.

In effect, with all of this “culture building,” JPMorganChase is its own strong “neural network”— powerful and healthy connections between our people. People usually look at investment as capital expenditures, but in many ways, our investment is in the intelligence of our people and their healthy connections. They need to perform like a well-functioning sports team. This network and the knowledge, talents and brainpower of our people, dedicated to the purpose of serving clients, create the capabilities that we have today, which would be very difficult to replicate.

A good culture is hard to create and easy to lose so you have to fight for it every day — with a little bit of grit, courage and an open mind.

We must remain clear-eyed: As good — or bad — as things feel now, we must necessarily always be prepared for all possibilities, including the possibility of some really tough times ahead. We do this so that our company is prepared to serve all of our clients, including governments around the world, regardless of the turn of events.

To do this, we look at many increasingly large and complex factors — such as geopolitics and wars, energy prices, trade and economic relations, political polarization, large global deficits and high asset prices, among others. We look at both short-term factors that will likely affect us in the ensuing 12 months and the complex factors that may affect us in the current year and in future years.

On Investor Day, our Chief Financial Officer showed what our returns would look like under various scenarios. Some of these examples reflect historical economic events. For instance, the worst-case scenario (a very bad recession) assumes front-end rates cutting to floor levels, the stock market dropping 40%, credit losses doubling and volumes dropping significantly. Even then, our return on tangible common equity would still be approximately 10%. It’s also worth remembering that the firm didn’t lose money in any single quarter during the great financial crisis — a period whose stresses are similar to those modeled for the Fed’s annual CCAR test. We are very disciplined in using both actual historical scenarios and very detailed economic models, but we know they do not and cannot accurately predict the future.

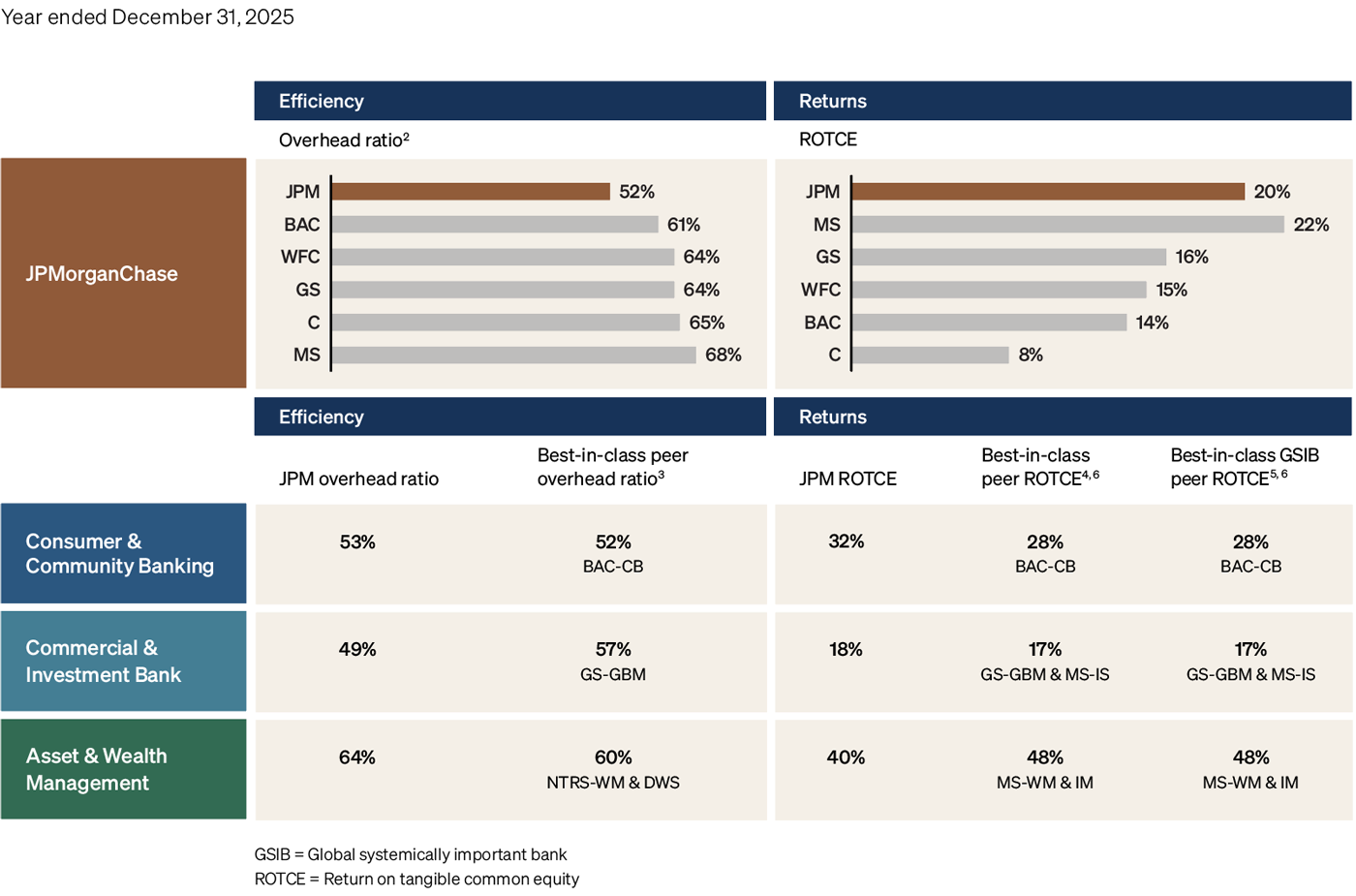

We often talk about our “through-the-cycle” target returns of 17% return on tangible common equity. By through the cycle, we mean that there will be times when returns will be better than that, and there will be times when they will be worse. We are often asked why we don’t raise that target since we have exceeded it for numerous years. It’s good to put this number in context. Compared with the returns of our 10 major competitors, this return has been exceeded only 9% of the time over the last 10 years.

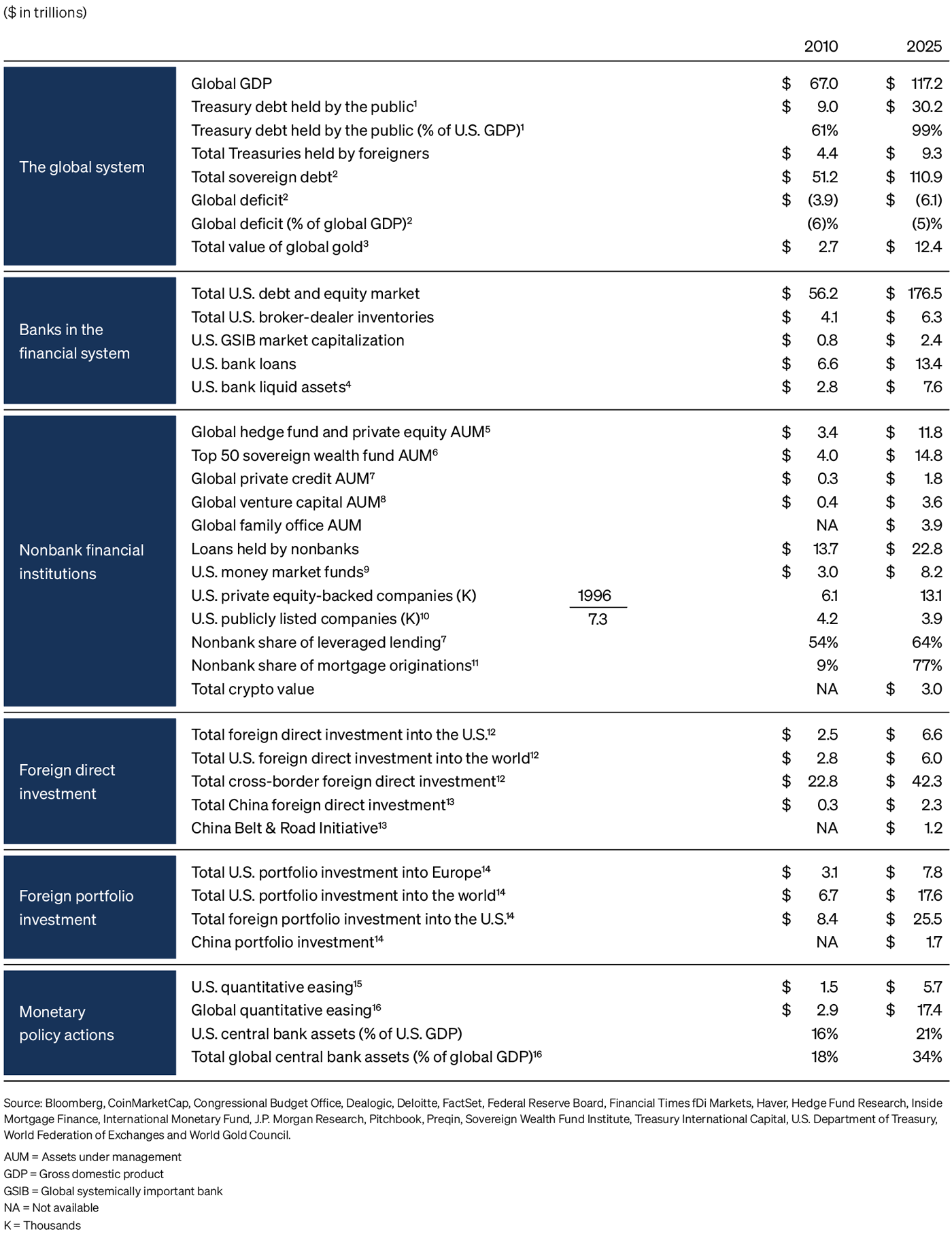

Before I talk about risks specifically, it’s helpful to recognize that the world’s economy is far larger and more diversified and far less reliant on energy as an input versus 20 years ago. Global energy consumption to the global gross domestic product (GDP) is only about 40% of what it was around 45 years ago, say in the early 1980s, and the United States, instead of being a major importer on a net basis, is now a major exporter. All of this may very well mean that the economy is more resilient and less vulnerable to some of the factors I am going to discuss. It is also good to remember that the United States remains the world’s best investment destination, particularly when things are going badly.

If you look at the table below, there are a few items that are truly different now from what they were in 2010, and these may well lead to different and unexpected outcomes. To name a few: The global debt and equity markets are far bigger than before (as are global deficits). Many nonbank financial institutions and investors are dramatically bigger than they were in the past (think hedge funds, private equity funds, sovereign wealth funds, among others). Global foreign portfolio investments are far bigger than before, and a large stock of U.S. Treasuries owned by foreigners is not held by central banks (central banks are less likely to make dramatic changes in their holdings of U.S. Treasuries). In addition, global QE is far bigger than it ever was before. A change in sentiment could easily affect the global flow of investments into securities, including U.S. Treasuries. You can also see that brokerage inventories are far smaller as a percentage of investments than ever before and, as a result, market makers are less able to intermediate in extremely volatile markets.

More broadly, as we think about how these new conditions relate to one another, it’s good to keep three things in mind: 1) It seems to me that while people frequently overreact to often-inaccurate short-term weekly and monthly data, their forecasts are generally small modifications versus current conditions, 2) while the economy may be less fragile than in the past, this alone does not mean there is no “tipping point” — it just may mean it could take more straws on the camel’s back to get there and 3) often it is an unexpected confluence of events that causes a “tipping point.” The convergence of rapidly increasing oil prices and inflation is frequently viewed as among the main causes of the very large 1974 and 1982 recessions. Also, human nature has not changed — sentiment and confidence can change rapidly and drive the markets.

Liquidity itself is a complex concept and can also change with sentiment. Often when people talk about liquidity, they are talking about the ability to readily buy or sell in the marketplace, e.g., when spreads are high and volumes are low, this would be considered low liquidity. Sometimes people are referring to the money supply. Money can be created by the central bank when it buys securities or by banks when they expand their balance sheets. In both cases, they create deposits (more liquid assets) in the short run. But all investors, from individuals to companies to major asset managers and banks, have their own liquidity needs and requirements, usually driven by their policy or regulatory policy, working capital requirements, collateral needs and sentiment (for example, the desire to be more conservative). When asset prices drop and all of these other factors change, the “need for liquidity” can change dramatically, too. When people get scared, they generally sell risky assets to buy safe ones, e.g., essentially T-bills or deposits at safe banks. And when they sell risky assets, they usually start with their most liquid positions.

While the most important outcome we should all hope for now is proper resolution of the current wars and, ultimately, peace on Earth, we do need to understand and track the economic effects of all the risks we mentioned. A bad confluence of events generally causes various degrees of a recession, which is accompanied by high credit losses and volatile markets, lower asset prices and higher unemployment rates, though recession would happen in different ways in different places. What might vary is inflation. There are some scenarios that would result in a recession, which generally reduces inflation, and other scenarios that would lead to a recession with inflation (stagflation — where inflationary forces overcome deflationary ones). The skunk at the party — and it could happen in 2026 — would be inflation slowly going up, as opposed to slowly going down. This alone could cause interest rates to rise and asset prices to drop. Interest rates are like gravity to almost all asset prices. And falling asset prices at one point can change sentiment rapidly and cause a flight to cash.

While there are many larger risks, as discussed in the next section, that may or may not impact the economy in 2026, we do know several things that will have a positive impact on the economy in the remainder of this year. They are:

Some of the items above have mild inflationary effects, while others probably have some deflationary effects.

I think some of the larger risks are much like tectonic plates, always moving and periodically causing earthquakes and volcanoes when they crash into each other. Some of the larger risks we should keep our eyes on are:

Private credit and credit in general. The leveraged private credit market totals $1.8 trillion. As a comparison, the U.S. high yield bond market totals $1.5 trillion, and the bank syndicated leveraged loan market totals $1.7 trillion. Taking a wider view, the total market size of investment grade bonds is $13 trillion. And the total market value of all residential mortgage securities and loans is also $13 trillion. In the great scheme of things, private credit probably does not present a systemic risk.

I do believe that when we have a credit cycle, which will happen one day, losses on all leveraged lending in general will be higher than expected, relative to the environment. This is because credit standards have been modestly weakening pretty much across the board; i.e., more aggressive and positive assumptions about future performance (called add-backs), weaker covenants, more use of PIK (payment-in-kind; not paying interest in cash but accruing it), more aggressive private ratings (particularly in insurance companies) and more arbitrage (not always a great sign). Also, by and large, private credit does not tend to have great transparency or rigorous valuation “marks” of their loans — this increases the chance that people will sell if they think the environment will get worse — even if actual realized losses barely change. Additionally, actual losses right now are already a little higher than they should be, relative to the environment. Finally, if rates or credit spreads ever go up, the companies that borrowed will have to borrow at even higher rates, putting them under even greater stress. However this plays out, it should be expected that at some point insurance regulators will insist on more rigorous ratings or markdowns, which will likely lead to demands for more capital.

It has always been true that not everyone providing credit is necessarily good at it. There are many players who are late to this game, and it should be expected that some credit providers will do a far worse job than others. We have not had a credit recession in a long time, and it seems that some people assume it will never happen.

Additionally, anything that gets sold to retail investors as opposed to institutional investors requires greater transparency, higher standards and fewer potential conflicts. If anything ever goes wrong, you should assume that retail investors, even though they were told about some of the risks, will seek remedy in the courts. Also, some of these loans go into various funds run by the asset management company. Generally, each of these funds has its own objectives and its own fiduciary responsibility to make sure that the loans are suitable for that specific fund. Those who do not do this properly are likely to get into trouble.

All in all, there are lots of moving parts and potential straws that might be added to the poor camel’s back. We are watching closely and hoping for the best. We always try to be prepared and vigilant and also recognize that tough times can create good opportunities.

There are three critical issues that will ultimately determine the health and safety of the United States and possibly determine the future direction and strength of the free and democratic world. JPMorganChase and its employees — like all other businesses and individuals — will be deeply affected over time by how the United States succeeds in these areas:

Foundational to accomplishing the three goals above is that the core strength of the United States — its deeply held values and principles, including our commitment to the Constitution — is constantly nourished and strengthened. In this section, we also ask and answer the question: What can we as a company offer in order to do our part?

Many public and private companies and institutions play a vital role in addressing various critical policy issues. The world is increasingly complex and polarized, and we need to remain completely clear-headed. It has become obvious, for example, that many of our largest policy issues cannot be solved by government or business alone. Our national security clearly depends not only on the U.S. military but also on the civilians and companies responsible for developing equipment and tools critical to our country’s defense, from ships and planes to chips and AI. JPMorganChase saw the benefit of collaboration in Detroit, where business leaders, community stakeholders and government officials worked together to successfully address the city’s economic decline. We see this same need for collaboration to help address challenges related to our national education system, job creation, skills development and virtually anything related to realizing the American Dream. America will be far stronger if more Americans prosper. The scale, brainpower and resources that institutions like ours can bring to bear on these challenges can be extraordinary.

We at JPMorganChase feel an enormous responsibility to our nation and many others — and we remind ourselves that many companies will only thrive if their countries thrive. With the right policies and committed actions, the United States will maintain the strongest military and strongest economy and will remain the bastion of freedom and the arsenal of democracy. (An important side note: This is also essential to maintaining the U.S. dollar as the world’s reserve currency.) In spite of all our extraordinary blessings, the United States needs to get stronger and tougher to make this true — no country has a divine right to success.

We have met big challenges before. At one point in 1940, only one nation, the United Kingdom, stood against the Nazi war machine, which had already conquered most of Western Europe. The United States was unprepared for what was going to happen but rose to the challenge. You may find it uplifting to read the book Freedom’s Forge, which shows how the United States came together to build the arsenal of freedom and to keep the world safe for democracy.

The ongoing war in Ukraine, the conflict between Iran and both the United States and Israel, and other major hostilities across the globe should permanently dispel the illusion that the world is safe. Having the world’s best military is expensive, but it will always be a huge deterrent to war. Fighting wars is even more expensive. And losing wars even more so.

I firmly hope that the United States provides sufficient military and economic support to help Ukraine prevail in what has become an extended and bloody war for democracy and against autocracy. Time will tell whether the current war in Iran achieves our short-term and long-term objectives in the region and at what cost. We should not turn a blind eye to the role the current regime in Iran has played in fostering terrorism and killing thousands of people, including Americans and many of its own citizens, over many years. And that threat must be addressed in an appropriate manner (by those who have more intel and knowledge than I do) — and urgently if Iran ever acquires a nuclear ballistic missile. Nuclear proliferation remains the gravest threat to the future of mankind.

The U.S. military umbrella has not only provided security for our allies and partner countries since World War II, but it has also provided safety and stability for non-allied states, including major countries like India.

While we have the world’s best military and while congressional oversight is a constitutional responsibility, the military is often stretched and hampered by congressional rules, interference, legislation and short-term budgeting, as well as by over-consolidation and under-investment in our defense industrial base. We need to spend more (and we hope smarter and more efficiently) on our military and give it the ability to move faster, unimpeded by politics and bureaucracy. The United States has also allowed itself to become too dependent on unreliable sources for items that are essential to our national security, such as critical minerals, semiconductors and advanced manufacturing output, among others. We have maintained insufficient productive capabilities to be ready to quickly increase production if necessary. And our military needs to be able to rapidly develop new and often cheaper weapons, like drones. The Pentagon, and in fact the whole government, is now actively addressing this problem, but it needs lots of private sector help.

JPMorganChase is well-positioned to do its part.

This initiative is a $1.5 trillion, 10-year plan to facilitate, finance and invest in industries critical to national economic security and resiliency. As part of this endeavor, we will make direct equity and venture capital investments, with an initial amount of $10 billion, to help companies enhance their growth, spur innovation and accelerate strategic manufacturing.

We are focusing our efforts on the following five key areas, supporting companies across all sizes and development stages by offering advice, providing financing and, in some cases, investing capital:

The initiative will also include special, thematic research focused on private industries and supply chain weaknesses like rare earths, AI and technology. It will be complemented by the firm’s recently launched JPMorganChase Center for Geopolitics, which provides us and clients with timely analysis and insights on top global trends. Policy is essential, too. So our objectives will include designing practices that can accelerate these efforts, including research and development (R&D), permitting reform, rapid and multi-year procurement, and regulations conducive to growth. As our firm intensifies its focus on those industries essential to our nation’s security and resiliency, we will also continue to work closely with our community and business partners to champion these enterprises, foster talent and support skills training to ensure companies can fill critical jobs.

Since the launch of our Security and Resiliency Initiative at the end of 2025, the response has been nothing short of remarkable. We have received more than 750 business opportunities from company leaders and government officials across critical sectors. To handle this momentum, we are assembling a dedicated 30+ person SRI global banking and investment team (supported by much of the rest of the company) with the experience and vision necessary to drive meaningful impact.

In addition, we announced the formation of an external advisory council composed of experienced leaders and exceptional thinkers from both the public and private sectors (from military generals to former secretaries of state and defense to business executives and CEOs) to help guide the SRI’s direction and strategy. I have the privilege of chairing this council, which recently convened in person in Washington, D.C., alongside many of JPMorganChase’s top leaders.

Building on advice from the advisory council, we are hosting our inaugural Defense Action Forum this month. Unlike typical industry conferences, our forum is designed to foster collaboration and generate practical solutions that drive meaningful change. The sessions will bring together leading experts to explore the pivotal role that the private sector can play in ensuring our nation's enduring strength and security. We hope to make some real progress, which will be shared broadly.

Our SRI work is more comprehensive than American security alone. This initiative will continue to be extended, as appropriate, to other allied nations. The SRI can help allied and partner countries and companies as they make the investments and reforms necessary to play a more active role in our nations’ common defense needs.

Over the last 20 years or so, U.S. GDP has averaged about 2% annually — I believe we could have easily achieved at least 3% growth. The reason we were able to grow 2% is that America’s businesses and entrepreneurial spirit allowed us to overcome a lot of the roadblocks mentioned later in this section. That 1% difference would have had an enormous impact, providing Americans with an extra $20,000 GDP per person annually, giving us resources to take care of nearly all our problems and jump-starting deficit reduction. Growth is part of the solution to almost all of our problems. Achieving such growth also would help restore trust in our government.

Good policy matters and is at the heart of sustainable progress. It’s policy, policy, policy. We’re committed to engaging with policymakers, supporting sound regulation, and advocating for growth and security. We’re investing in strong policy teams and backing our positions with rigorous analysis. We have a responsibility to help shape the right policies, not just for our company but for the country and the world.

In the Sturm und Drang of today’s politics, you mostly hear about simplistic solutions like raising taxes, taxing the rich and cutting expenses, but as any businessperson knows, you should always be asking, “How are you doing with what you have?” Our inefficiencies, red (and blue) tape and lack of analysis stifle our growth and almost always hurt the poor the most. But there are so many things that could be done that could make everything better — for all citizens. And these things would be virtually free.

I am going to mention a few damaging policies, not in detail because I’ve written about them in the past, but if they aren’t corrected, real progress may be impossible.

Mortgage and regulatory policies and local housing requirements. Excessive rules around mortgages (servicing, origination and securitization) have pushed most of the mortgage business out of banks and have increased the cost of mortgages by 20–30 basis points. Mortgage regulatory reform alone would make the mortgage business far safer and generate an additional 500,000 mortgages a year. Local zoning requirements often limit affordable housing and make it much more expensive. In addition, there are many examples of excellent public/private affordable housing programs, which only need to be replicated.

Fixing these regulations would go a long way to helping people achieve this part of the American Dream.

Red and “blue” tape, permitting reforms and a little litigation reform. Some politicians think that all regulations are good — the more the better. Given that many of these politicians come from the blue side of America’s red-blue divide, I think it’s more appropriate to call excessive regulation “blue tape.” We should aim for “good” regulations, continuously improved, to both protect the public and reduce costs. You probably need to have real-life experience in dealing with regulations to understand this.

Permitting and many associated regulations take too long and not only extend the duration of a project but also increase the cost and sometimes stop projects from beginning. Many countries, including Canada and Singapore, have successfully introduced policies to dramatically reduce permitting time.

Proper federal, state and local regulations, along with permitting reform, are necessary to reduce delays and legal bottlenecks. Minimizing “blue” tape — excessive regulatory and related litigation costs — would make it easier, cheaper and faster to build infrastructure such as roads, schools, bridges, energy facilities and housing. A little common sense would go a long way.

One last point: Excessive regulations make it much harder to start a new business, and they often reduce competition. And they almost always hurt smaller companies more than larger ones.

Failure to recognize that capital formation drives growth. Central to growth in a country and growth of its GDP are capital formation and disciplined capital allocation. Countries that do not promote capital formation, including those that tolerate policies inhibiting capital formation, fail to thrive. Globally competitive taxes and policy certainly are critical for capital formation. Other good policies include strengthening active capital markets, tax incentives for capital expenditures and R&D, and savings and pension plans (we support the new “Trump Accounts” that, over time, will give all Americans an economic stake in America) that incent investment in equities, venture capital and other investments.

There are also some good examples found in other countries. In Sweden, an investment savings account is available that simplifies the investing process with favorable tax treatment. Account holders can deposit and withdraw funds at any time, and there is no capital gains tax — just an annual tax of 1% on the balance. This has dramatically increased investment by retail investors into the Swedish stock market. It may surprise some of our readers that Sweden’s policies have created a growing and innovative stock market and that Sweden has more unicorns and billionaires per person than America does. Another example is Australia, which has a wonderful retirement policy based on superannuation, a savings account funded by both employer and employee contributions.

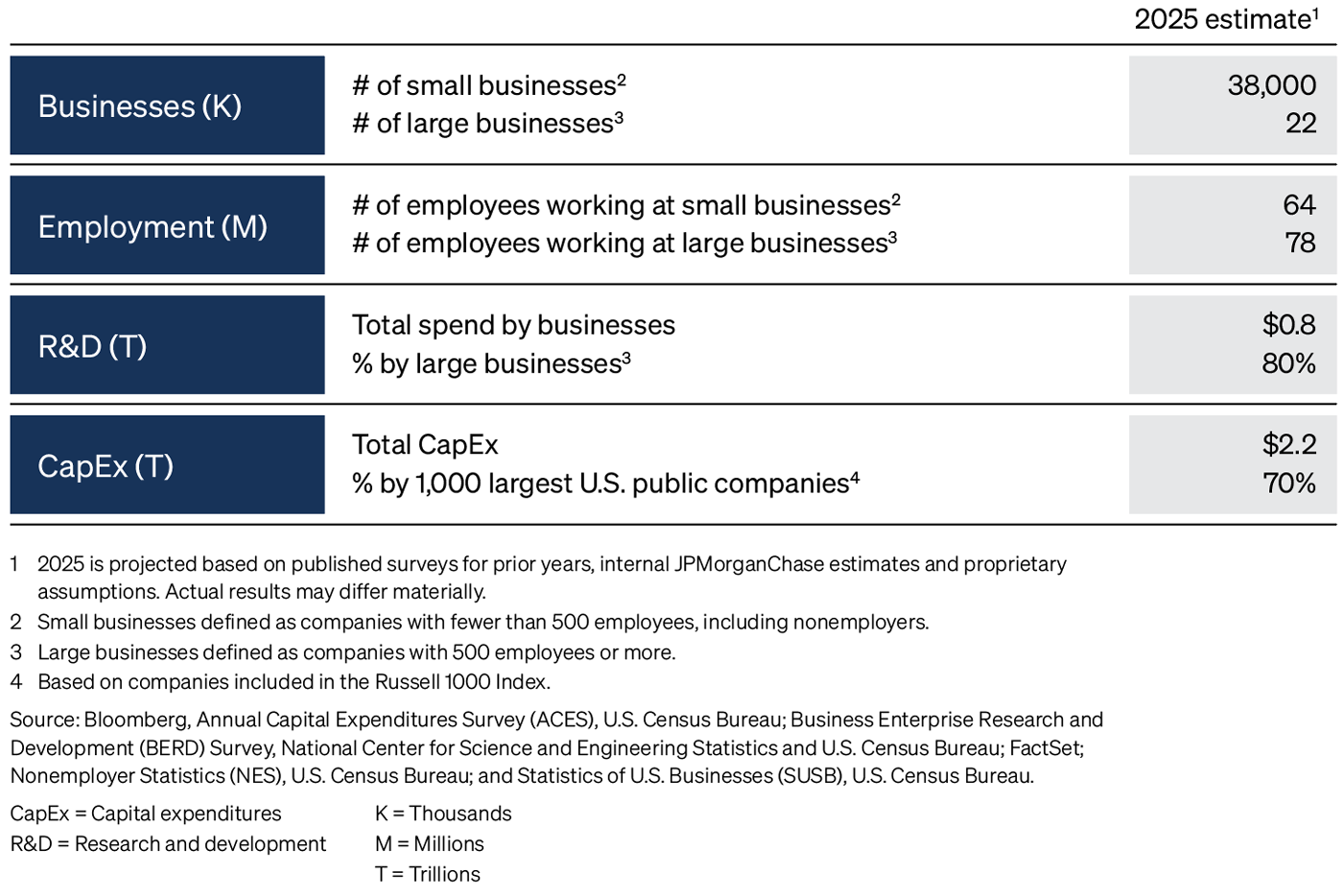

We must recognize that capital formation drives capital expenditures and R&D, and large companies lead the way: 80% of R&D is done by large companies; and 70% of capital expenditure comes from the largest 1,000 public companies. This is what drives productivity and GDP-per-person growth. And small business and big business are symbiotic. When a bigger company builds a billion-dollar plant that creates 5,000 jobs, it may also generate 25,000 jobs surrounding the facility. These jobs are often small businesses that are developed to support the plant and those who live nearby.

People often refer to financialization of the economy as a bad thing — and if they mean pure speculation, then I understand. But a country that is a barter economy effectively has no financial assets. As capital formation takes place, financial assets, including stocks, bonds and loans, are created, which represent all the investment. And as a country grows and continually reinvests in higher productivity, there will be more financial assets per person. While the market value of those assets may fluctuate, the growth in financial assets is very good.

The American Dream itself rests upon our providing, as best we can, equal opportunity to all our citizens. Education and jobs are still the best way to achieve this. Much of our education system no longer truly meets our country’s promise that its students graduate with the skills they need to attain a good job.

In a number of our inner city and rural high schools, under 50% of the students graduate, and those who do often don’t have the skills they need to hold a well-paying job. Increasingly, poverty has become intergenerational.

The growth of America was always driven by productivity that matched capital investment with skills, which is also the driver of individual income. Fortunately, to fix our problems, all we need to do is reorient what we do today. No investment is required. It is essentially free; we just need to redirect existing resources (the United States spends almost $1 trillion a year on K–12 education) into better outcomes.

We know exactly what to do, though systems change is hard. There are millions of jobs available for which training could be done in high school, community college or special programs outside of school. For example, there are training programs lasting 12–24 weeks in computer science, advanced manufacturing, cyber, data science, program management, and nursing and healthcare-related areas, among others. These trainings should be certified and counted as credits for an undergraduate or graduate education. Many unions run excellent apprenticeship and training programs that certify workers for badly needed high-skilled jobs like welding, electrical work, plumbing and others. These jobs can pay well in excess of $100,000 a year.

The federal government should use its considerable power to ask every school to report on the jobs and income levels that their students achieve when they leave school. This alone would put tremendous pressure on schools to become accountable — everyone would be seeking out best practices so as not to be left behind. I would even consider tying teacher and administrator compensation to these goals.

It is clear that, over the decades, the income levels of low-wage workers have not kept up with general growth and overall salaries despite the fact that their work is still essential. It is also clear that in any economy, there are groups of people who are struggling to get ahead. Approximately 23% of American workers make less than $17 an hour. And close to 10% have an income of $20,000 a year or less, partially because they only have part-time jobs. Some surveys show that over 60% of workers today are living paycheck to paycheck, that hourly workers have less predictable incomes and that 35% of households with incomes below $50,000 spend 95% on necessities these conditions are likely very stressful for many families. We need to fix this.

Dramatically expanding the Earned Income Tax Credit (EITC) does not help everyone, but it would go a long way in helping those who need it most. The tax code could play an important role in easing the stress of individuals and families at the bottom of the economic ladder. One way the code could incentivize labor force participation is to expand and reform the EITC. The EITC gives an individual earning $18,000 a year with two children a maximum tax credit of $7,152 (and with no children a maximum tax credit of $649). The average EITC across all recipients is approximately $2,900, and close to 20% of eligible taxpayers don’t apply. I would double this tax credit and remove the child requirement. I would effectively make it a negative monthly income tax as opposed to a year-end credit. (It’s also important that any tax credit and social benefits program be properly phased in so it is both fair and it doesn’t dis-incent work.)

While this would cost a lot of money, it has many excellent virtues. It would give those with lower income far more money to spend, without government interference, on what they and their families need — education, food, better housing and so on. And much of it would be spent locally, in lower-income neighborhoods. This plan has the benefit of both rewarding work and bringing more people into the workforce, which would grow GDP. Jobs not only bring dignity but better social outcomes in terms of less homelessness and crime, improved health outcomes and more household formation, among other upsides. For many people, that first job is just the first rung on the ladder of a career. I have little doubt that this plan would more than pay for itself over time. Many Republicans and Democrats support this proposal as it helps to create the American Dream for many people.

Uncontrolled immigration is highly disturbing to affected populations around the world and reduces the ability to manage legal and needed immigration. In the United States, the number of immigrants has increased by more than 60% over the last 25 years. Since we have finally gained control of our borders, I believe most Americans would support the following: increasing merit-based immigration, allowing anyone who earns a degree here to stay, ensuring there are proper visas for seasonal workers, enabling children born in this country to remain and providing a rigorous path to citizenship for law-abiding, undocumented immigrants.

Healthy and proper immigration would bring great talent to our country and has been shown to actually help grow the economy. There are over 150,000 foreign students who receive a degree annually in science, technology, engineering or math but have no guaranteed way of staying here for the long term, although many would choose to do so. Most students from countries outside the United States pay full freight to attend our universities, but many are forced to take the skills they learned here back home. From my vantage point, that means one of our largest exports is brainpower.

The last time we had major immigration reform was in 1986 under President Reagan. There have been two times in the last 20 years when Congress almost passed an immigration reform bill that looks a lot like what I outlined above. Let’s just get it done this time.

The Congressional Budget Office estimated that the failure to pass immigration reform is costing us 0.3% of GDP a year. Immigration has been one of the great strengths of this country — we should never forget that.

The goal of U.S. economic foreign policy should be twofold (after protecting national security):

Economic weakening of the world’s democracies or a fragmentation of their economic bonds could lead to truly adverse consequences. This is precisely what some of our adversaries and many autocratic nations want — it is their stated objective. They would like to see all of our allies far less dependent on the United States and therefore far more dependent on them. In this scenario, many countries would be compelled to seek deeper economic bonds with some possible bad actors — over time, they could become vassals of these countries and unable to avoid coercion from them. The following are a few ideas on how we can promote healthy economic engagement (and combat unfair trade) while strengthening both our own and our allies’ economies. And I will leave you with one big, bold idea.

America’s ties with the rest of the world are already extensive (see U.S. global foreign direct investment and portfolio investment), and the levers to accomplish our foreign policy goals extend to tax policy (and our international competitiveness), investment policy and trade policy, which encompass tariffs, quotas, regulatory barriers, immigration policies and so on. While tariffs have certainly “brought people to the table” and have allowed us to start to correct some of our past bad trade practices, we need to look at U.S. foreign economic policy comprehensively. The ultimate goal should be to create a system with our allies of stability and consistency, in addition to fairness and mutual benefit.

Not only should our foreign economic policy help us grow as a nation, but it should also help other countries grow. For example, the United States has the best capital markets in the world, large and small, public and private, and we have already described how proper capital formation and allocation are key to America’s vibrant economic system. Another goal of our foreign economic policy should be to help other countries develop their capital markets. In addition, there are excellent economic policies found elsewhere in the world, and we should emulate them to help more countries thrive.

Even the proper use of strategic communications can foster entrepreneurship and the universal principles of freedom, which will also drive growth and prosperity.