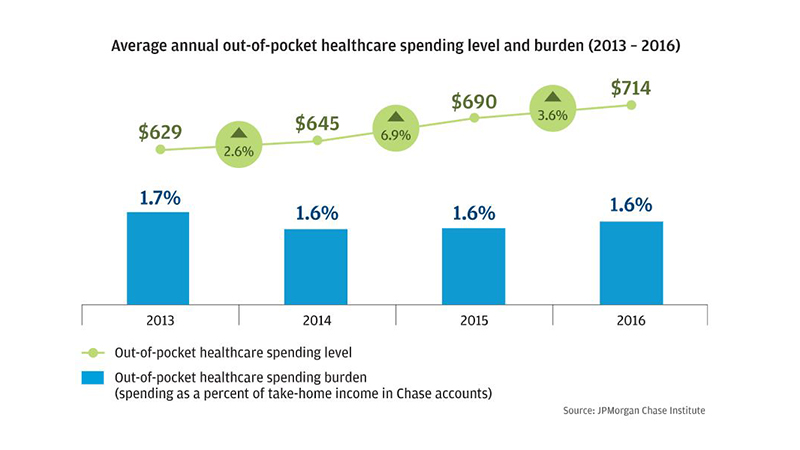

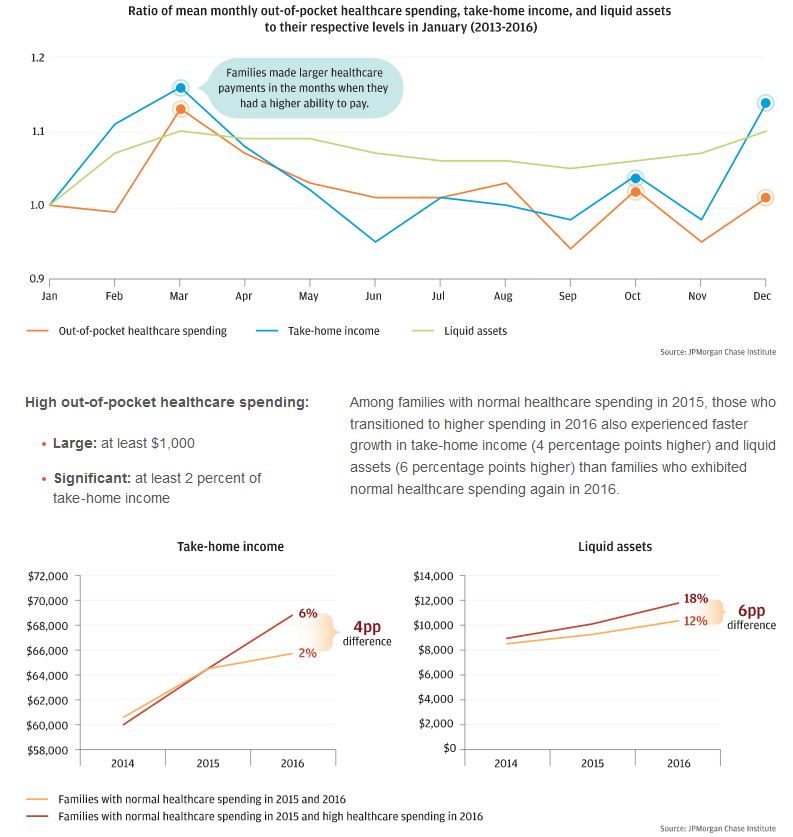

Executive summary Data

Healthcare costs are rising for families. In 2015, the US spent 18 percent of Gross Domestic Product (GDP) on healthcare, up from 13 percent in 2000. For every dollar spent on healthcare, families paid 11 cents out-of-pocket and 28 cents after including insurance costs. While the Centers for Medicare and Medicaid Services projects health spending to continue to grow faster than GDP through 2025, the future of family-paid healthcare costs also rests with policy choices currently being debated. Out-of-pocket costs are a key piece of that picture.

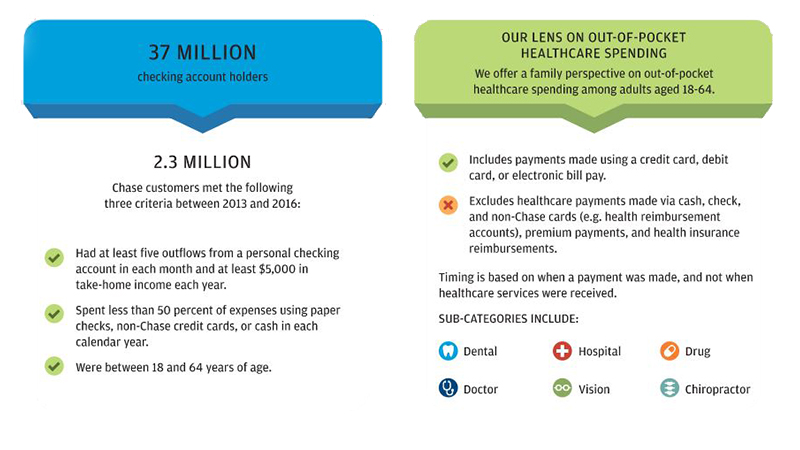

The JPMorgan Chase Institute set out to better understand out-of-pocket healthcare spending among US households. Building off a sample of 2.3 million de-identified core Chase customers aged 18 to 64 between 2013 and 2016, we created the JPMorgan Chase Institute Healthcare Out-of-pocket Spending Panel (JPMCI HOSP). We explored the levels, concentration, and growth of out-of-pocket healthcare spending and the implications of these spending trends for overall household financial health. The JPMCI HOSP provides a first-ever look into out-of-pocket healthcare spending for households on a month-to-month basis, at the state, metro, and county level, and as recent as 2016. In this report, we describe the creation of, and initial insights gleaned from, this new data asset.