City and regional governments spend considerable time promoting their cities to international markets whether for exports of goods or as a tourist destination. Overlooked is the importance of domestic visitors—business travelers, tourists, or day-trippers—who allow a metro area to extend its economic reach. Much as exports enable firms to reach new markets and consumers beyond their immediate surroundings, increasing the number of visitors to a metro area increases the number of potential customers. Visitors are important beyond the traditional tourist-centric sectors such as hotels or restaurants, with purchases extending into retail and entertainment amongst others. Leveraging data from 12.4 billion anonymized credit and debit card transactions in 15 metropolitan areas, the JPMorgan Chase Institute's recently released Profiles of Local Consumer Commerce (PLCC) can help better explain spending by domestic visitors in metropolitan areas.

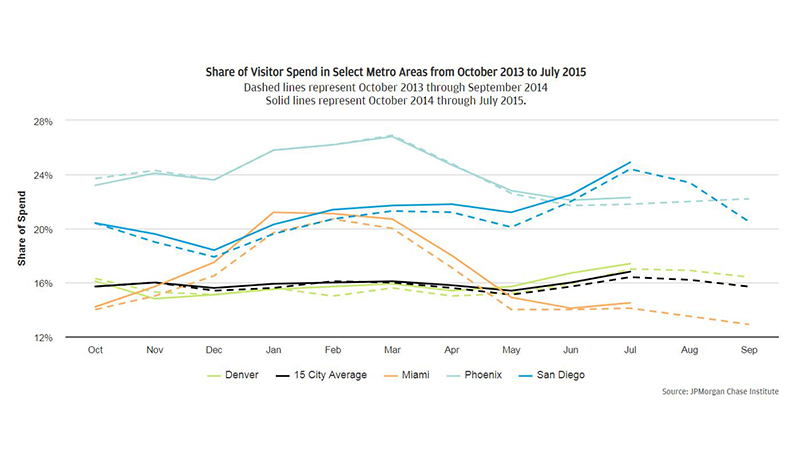

Across the fifteen metro areas, the average share of spending by nonresidents was 15.6 percent of total consumer spending. The average masks considerable variance across the cities, as shown in the table below. In Phoenix, nonresidents accounted for 23.0 percent of all local consumer commerce spending. This is nearly 17 percentage points higher than the city with the lowest share of spending by nonresidents, Houston, where visitors only accounted for 6.1 percent of spending. Besides Phoenix, other cities at the top of the rankings include San Diego and Seattle.