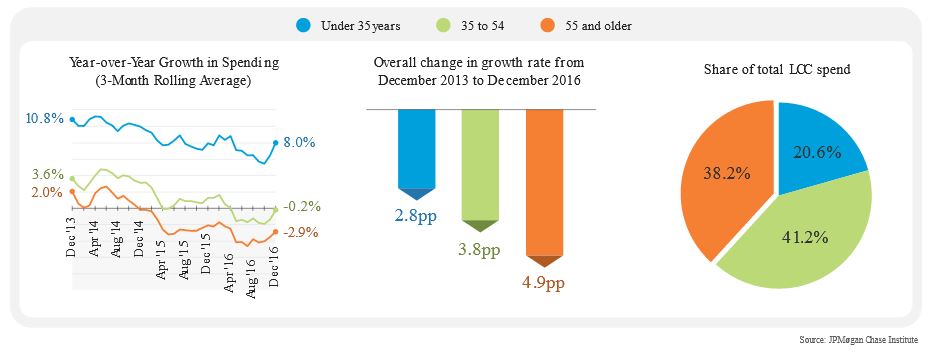

The share of total spending by older consumers is large enough that growth declines within this group can affect the overall growth rate (see Figure 1). In December 2016, consumers between the ages of 35 and 54 and consumers 55 and older made up 41.2 percent and 38.2 percent of total LCC spend, respectively. In contrast, consumers under 35 only made up 20.6 percent of total LCC spend in the same time period.

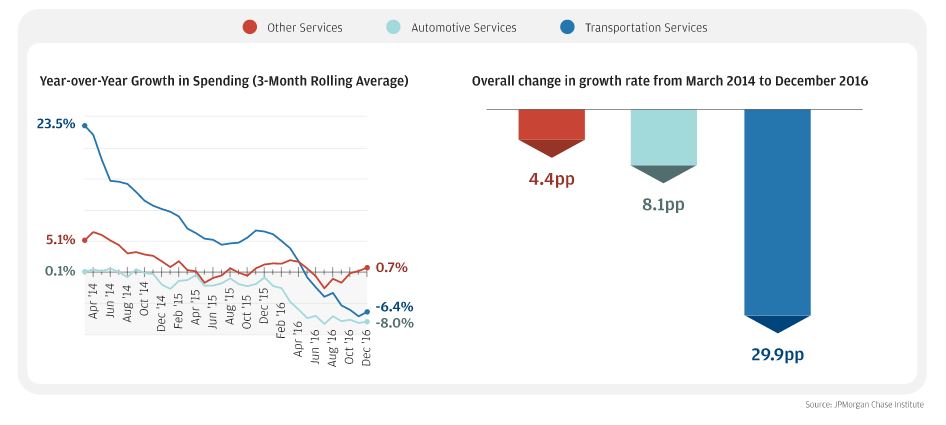

Older consumers generally have lower spending growth relative to their younger counterparts across all product types. However, to better understand which age groups have driven the overall decline in spending growth, we focus on the gap between growth rates. While this gap has been fairly stable across most product types over time, spending growth on restaurants (17 percent of total LCC spending) and other services (15.7 percent of total LCC spending) have seen a widening gap.