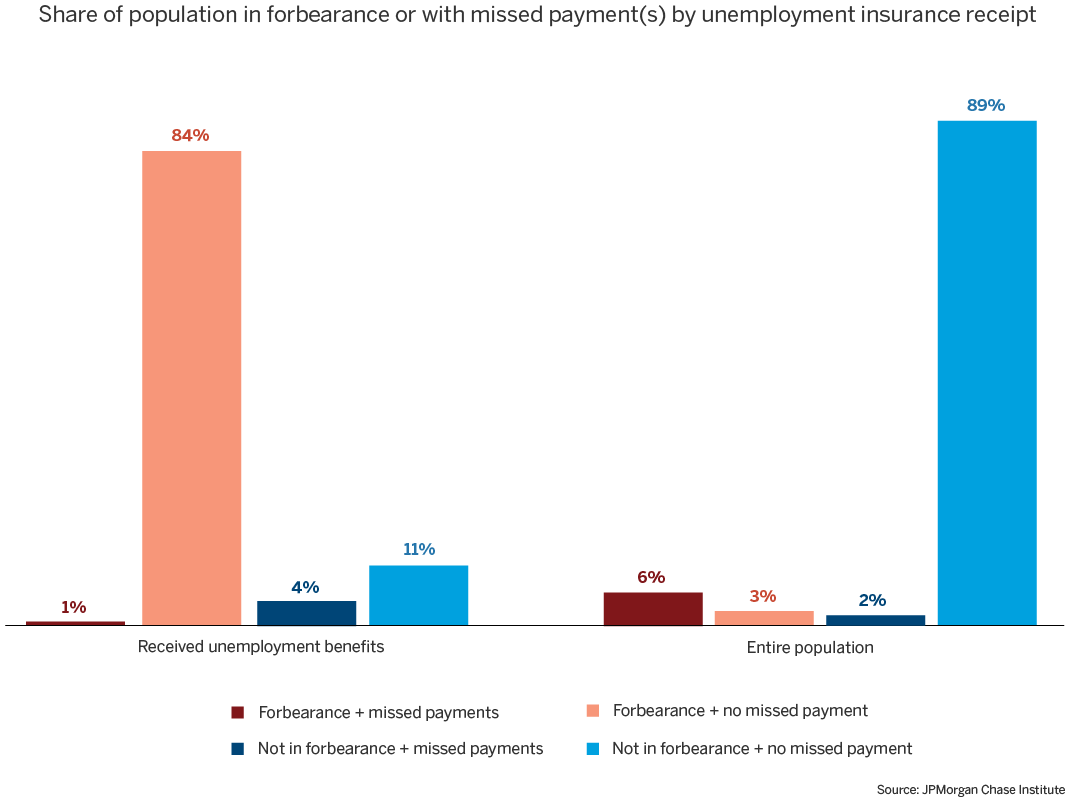

Figure 1: Those who lost their jobs and were receiving unemployment insurance overwhelmingly opted into forbearance but did not use it.

Latest news

An Ohio-based company is protecting first responders around the world

With support from JPMorganChase, Fire-Dex is providing protective equipment to firefighters in 100 countries and all 50 states.

Learn moreLatest news

Veteran’s Unconventional Path to Landing her Dream Job in Tech

U.S. Army Veteran Ashley Wigfall transitioned to a civilian role and charted her path to technologist through mentorship and skills training at the JPMorgan Chase tech hub in Plano, Texas.

Learn more

A central question for any government assistance program is how to reach the people who need help as quickly as possible while also making sure that those who receive help actually needed it?

Studies show mortgage forbearance programs that require no documentation were largely utilized as intended by homeowners.

Recent JPMorgan Chase Institute research examined this question in the context of mortgage forbearance.1 Early on in the COVID-19 pandemic, the Coronavirus Aid, Relief, and Economic Security (CARES) Act provided most homeowners with up to a year2 of payment relief if they attested to a COVID-related hardship with no documentation requirement. Using administrative mortgage servicing and checking account data, we found little evidence of moral hazard associated with the program.

Borrowers using forbearance to miss mortgage payments had larger drops in income than other homeowners and experienced income changes similar to those who became delinquent without the protection of forbearance. In addition, borrowers in forbearance were more likely to have lost labor income and received unemployment benefits than borrowers not in forbearance. In fact, of those we can observe receiving direct-deposited unemployment insurance (UI), 84 percent were in forbearance and continuing to make their mortgage payments and only 1 percent were in forbearance but missing mortgage payments. In other words, almost all of those who received UI and signed up for forbearance continued to make mortgage payments when they were able to.3 (Figure 1)

Figure 1: Those who lost their jobs and were receiving unemployment insurance overwhelmingly opted into forbearance but did not use it.

In contrast, Great Recession-era programs with strict documentation requirements suffered from low uptake.

During the Great Recession, programs aimed at helping struggling homeowners came with significant documentation requirements. Studies have since shown that those requirements hampered the success of many of these programs. The Hardest Hit Fund (HHF) was established in 2010 to offer mortgage payment assistance for unemployed or underemployed homeowners. By the end of 2016, only 292,000 homeowners had benefited from the HHF. The Home Affordable Unemployment Program (UP) was introduced in 2010 to provide assistance to unemployed homeowners who were unable to make their mortgage payments. At of the end of 2016, only 46,485 homeowners were participating in the UP program.4 Similarly, mortgage modification programs such as the Home Affordable Modification Program (HAMP) also had low uptake. Between March 2009 and June 2010 about 55 percent (almost 675,000) of HAMP trial modifications were cancelled because homeowners could not provide the requisite income verification documentation.5 By April 2015, more than one million homeowners had been denied a HAMP modification because they did not provide the financial and/or hardship verification documentation required to complete the evaluation of their request in a timely manner.6 Finally, research has shown that similar requirements associated with refinancing programs during this time (e.g., the Home Affordable Refinance Program) limited uptake to less than 50 percent of eligible borrowers. As a result, these refinancing programs had modest effects on foreclosure rates.7

JPMC Institute data also show little evidence of strategic default among homeowners

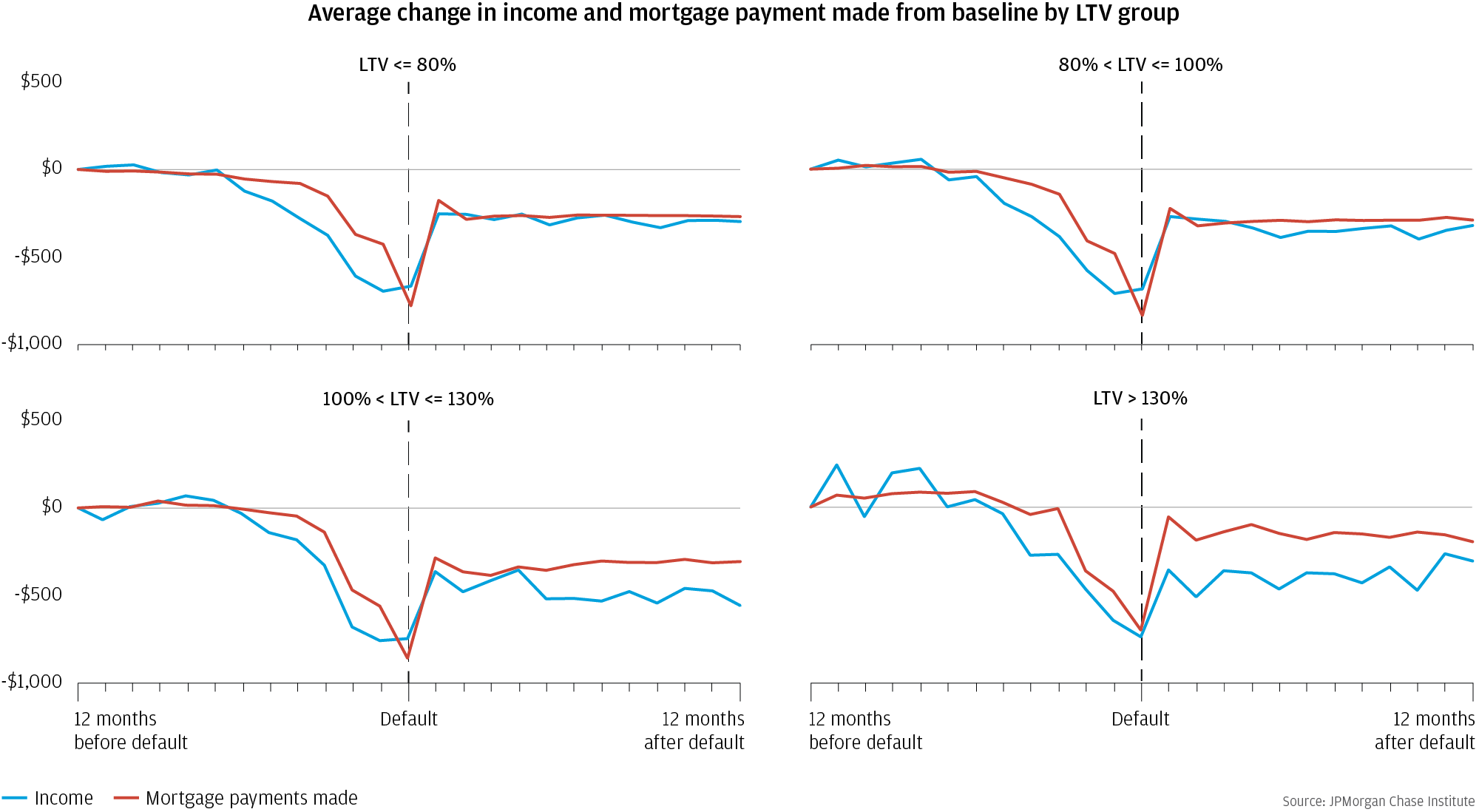

During the Great Recession, many homeowners were underwater and policymakers were worried about strategic default—the risk that homeowner would walk away from their debt obligation once the mortgage exceeded the value of their home. Evidence suggests, by and large, homeowners did not do this. Using mortgage servicing and deposit account data, JPMC Institute research shows that for borrowers who defaulted on their mortgage, default closely followed a negative income shock regardless of their level of home equity. This was true even when the homeowner was deeply underwater.8 (Figure 2) This result is inconsistent with the simple type of strategic default described above. Ganong and Noel (2020), using JPMC Institute data, compare underwater borrowers to a group with no strategic default motive: borrowers with positive home equity. They find that only 3 percent of defaults are caused exclusively by negative equity and that adverse events are a necessary condition for 97 percent of mortgage defaults.9 This suggests that homeowners see their homes as more than a financial asset and place a high priority on being able to remain in their homes.

Figure 2: Default followed a negative income shock for borrowers across the LTV distribution, providing suggestive evidence against a simple model of strategic default where deeply underwater borrowers stop making mortgage payments only because they are underwater.

Renter assistance programs are fundamentally different from mortgage forbearance programs but may also see low take-up if documentation requirements are too onerous

JPMC Institute research has shown that compared to mortgage holders, renters were on weaker financial footing prior to the pandemic and experienced greater job losses and labor income declines during the pandemic. Furthermore, even though generous expansions of UI and EIP checks increased total income for many renters, more than one in five saw their total income decrease by more than 10 percent. Finally, renters entered the pandemic with much lower levels of savings and their relative position did not improve meaningfully during the pandemic despite government stimulus programs as they depleted more of the stimulus-generated additional savings by the end of the year than mortgage holders. Importantly, these results likely represent a “best case scenario” for renters since Institute data capture a sample of renters that skew higher in income. An analysis that includes more low-income renters—especially those that are underbanked or already struggling with housing payments—would likely show worse financial outcomes for renters.10 These results point to renters needing some form of rental assistance.

While rental assistance programs already existed in some specific localities, the main form of rental assistance during the pandemic arrived in December 2020 with the Consolidated Appropriations Act of 2021, which established a $25 billion Federal Emergency Rental Assistance Program for state and local governments. In order to apply for this program, renters were required to fill out forms and upload documents proving unemployment or income loss, risk of homelessness or housing instability, and income that did not exceed 80 percent of area median income (AMI).11 Such extensive requirements may, similar to the housing assistance programs of the Great Recession, result in many renters unable to access assistance because they are unable to demonstrate their need (e.g., they require assistance filling out the application forms, their income is difficult to document, etc.). It is worth acknowledging that rental assistance is fundamentally different from mortgage forbearance: rental assistance provides a transfer of money to renters, while forbearance is a deferral of a debt obligation. Additionally, renters may exhibit different behavior than homeowners when it comes to housing payments. That said, the research around moral hazard and uptake for mortgage forbearance and Great Recession-era housing programs is still instructive. As such, policymakers may consider revisiting whether the right balance between accessibility and fraud prevention has been found in rental assistance programs.

Farrell, Diana, Fiona Greig, and Chen Zhao. 2020. "Did Mortgage Forbearance Reach the Right Homeowners? Income and Liquid Assets Trends for Homeowners during the COVID-19 Pandemic." JPMorgan Chase Institute.

The Biden administration extended this by an additional 6 months.

Undoubtedly, unusually generous unemployment insurance payments during COVID allowed these families to continue making mortgage payments.

Source: Making Home Affordable Program Performance Report through the Fourth Quarter of 2016, https://www.treasury.gov/initiatives/financial-stability/reports/Documents/MHA%20 Quarterly%20Report%20Q4%202016_C.pdf.

During the earlier phase of the program, borrowers who were put into trial modifications based on stated information and then did not provide documentation verifying that information had their modifications cancelled.

As noted in the SIGTARP July 29, 2015 Quarterly Report to Congress (see https://www.sigtarp.gov/Quarterly%20Reports/July_29_2015_ Report_to_Congress.pdf) and the MHA Q4 2016 Performance Report (see https://www.treasury.gov/initiatives/financial-stability/ reports/Documents/MHA%20Quarterly%20Report%20Q4%20 2016_C.pdf).

Agarwal, Sumit, Gene Amromin, Souphala Chomsisengphet, Tim Landvoigt, Tomasz Piskorski, Amit Seru, and Vincent Yao. Mortgage refinancing, consumer spending, and competition: Evidence from the home affordable refinancing program. No. w21512. National Bureau of Economic Research, 2015.

Farrell, Diana, Kanav Bhagat, and Chen Zhao. 2018. “Falling Behind: Bank Data on the Role of Income and Savings in Mortgage Default” JPMorgan Chase Institute.

Ganong, Peter, and Pascal J. Noel. Why do borrowers default on mortgages? A new method for causal attribution. No. w27585. National Bureau of Economic Research, 2020.

Greig, Fiona, Chen Zhao, and Alexandra Lefevre. 2020. " Renters versus Homeowners: Income and Liquid Asset trends during COVID-19." JPMorgan Chase Institute.

https://home.treasury.gov/policy-issues/cares/emergency-rental-assistance-program