- The Firm delivered strong underlying performance for the quarter2

- Consumer & Community Banking: average Consumer & Business Banking deposits up 9%; credit card sales volume1 up 12%; record client investment assets up 16%; Business Banking loan originations up 27%

- Corporate & Investment Bank: maintained #1 ranking for Global Investment Banking fees with 8.0% wallet share YTD; assets under custody up 8%

- Commercial Banking: period-end loan balances up 6%, driven by 13% growth in Commercial Real Estate; record YTD gross investment banking revenue with Commercial Banking clients up 22%

- Asset Management: twenty-second consecutive quarter of positive net long-term client flows; assets under management up 11%; average loan balances up 16%

- Third-quarter results included as a significant item $1.0 billion after-tax Firmwide legal expense3 ($0.26 per share after-tax decrease in earnings; $1.1 billion pretax expense)

- Approximately $3.0 billion returned to shareholders in 3Q14

- Repurchased $1.5 billion of common equity4

- Common stock dividend of $0.40 per share

- Core loans1 up 7% compared with the prior year

- JPMorgan Chase supported consumers, businesses and our communities

- $1.6 trillion of credit and capital1 raised for the first nine months of 2014

- $145 billion of credit for consumers

- $15 billion of credit for U.S. small businesses

- $464 billion of credit for corporations

- $881 billion of capital raised for clients

- $55 billion of credit and capital raised for nonprofit and government entities, including states, municipalities, hospitals and universities

- Hired over 7,700 U.S. veterans and service members since 2011

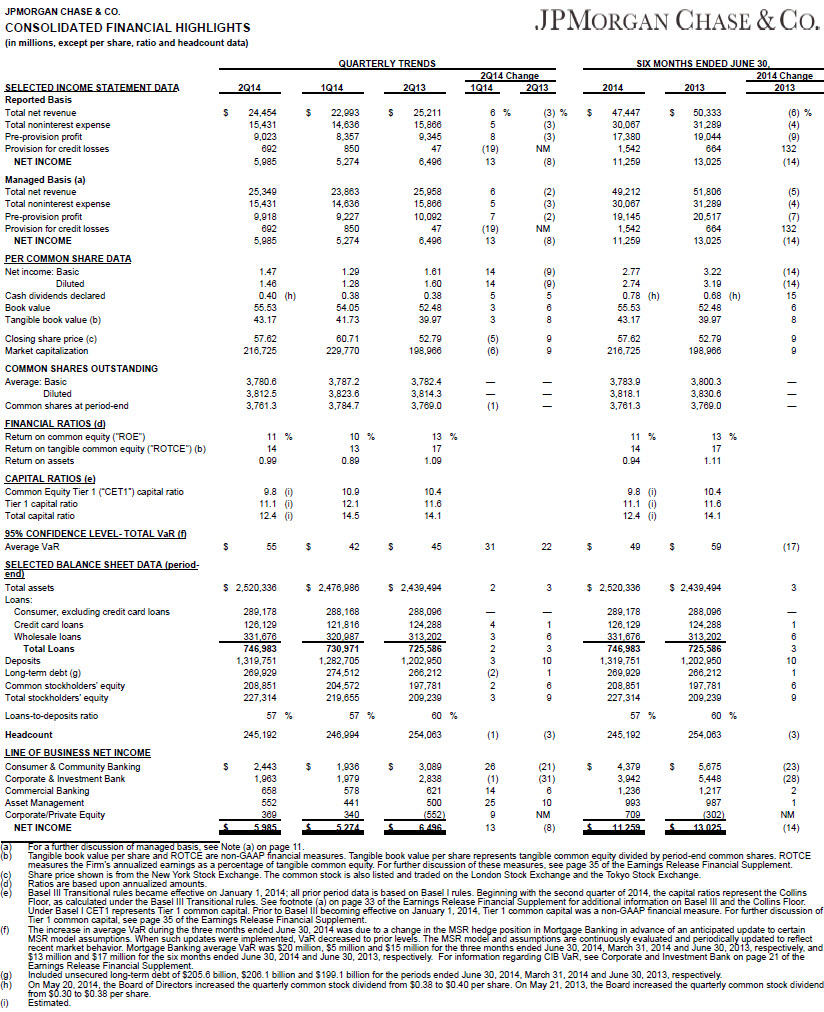

New York, October 14, 2014 - JPMorgan Chase & Co. (NYSE: JPM) today reported net income for the third quarter of 2014 of $5.6 billion, compared with a net loss of $0.4 billion in the third quarter of 2013. Earnings per share were $1.36, compared with $(0.17) in the third quarter of 2013. Revenue1 for the quarter was $25.2 billion, up 5% compared with the prior year. The Firm's return on tangible common equity1 for the third quarter of 2014 was 13%. Core loans1 increased by 7% compared with the prior year. The Firm repurchased $1.5 billion of common equity4 in the third quarter.

Jamie Dimon, Chairman and Chief Executive Officer, commented on the financial results: "Our businesses continue to perform well. Consumer & Community Banking deposit growth led the nation as the FDIC reported Chase #1 in deposit growth for the third consecutive year. Our Card business delivered double-digit sales volume growth and Mortgage Banking continues to reposition the business and manage through cyclical-lows.

The Corporate & Investment Bank saw strong performance in fees, maintaining a #1 position in Global IB fees year to date, with particular strength in equity capital markets. In Markets, we saw increased activity and better performance overall, particularly in currencies and emerging markets. In Commercial Banking, strong competition in the industry for quality assets resulted in some spread compression. However, our Commercial Banking clients leveraged the services of our investment bank, generating record investment banking revenues year to date, and growth in Commercial Real Estate remains strong. Lastly, Asset Management saw its twenty-second consecutive quarter of long-term inflows, record net income and strong margins."

Dimon continued: "While challenges remain in the global economic recovery, the U.S. economy is an exception, showing signs of steady improvement. Corporate America is in good shape with strong balance sheets and employment trends continue to be positive. JPMorgan continued to support the economic recovery. We provided credit and raised capital1 of $1.6 trillion for our clients during the first nine months of 2014, which included $15 billion for U.S. small businesses."

Dimon concluded: "Despite challenges, we have continued to deliver strong underlying performance, maintain our fortress balance sheet and liquidity, simplify the business and adapt to regulatory changes. We remain very focused on executing the control agenda and investing to protect our customers and the company for the future."

In the discussion below of the business segments and of JPMorgan Chase as a Firm, information is presented on a managed basis. For more information about managed basis, as well as other non-GAAP financial measures used by management to evaluate the performance of each line of business, see page 12. The following discussion compares the third quarters of 2014 and 2013 unless otherwise noted. Footnotes in the sections that follow are described on page 13.

CONSUMER & COMMUNITY BANKING (CCB)

| Results for CCB ($ millions) | 3Q14 | 2Q14 | 3Q13 | 2Q14 | 3Q13 |

|---|

| $ O/(U) | O/(U) % | $ O/(U) | O/(U) % |

|---|

| Net Revenue | $ 11,267 | $ 11,431 | $ 11,082 | $ (164) | (1)% | $ 185 | 2% |

| Provision for Credit Losses | 902 | 852 | (267) | 50 | 6 | 1,169 | NM |

| Noninterest Expenses | $ 6,305 | $ 6,456 | $ 6,867 | $ (151) | (2) | (562) | (8) |

| Net Income | $ 2,468 | $ 2,443 | $ 2,702 | $ 25 | 1% | (234) | (9)% |

Discussion of Results:

Net income was $2.5 billion, a decrease of $234 million, or 9%, compared with the prior year, due to higher provision for credit losses, largely offset by lower noninterest expense and higher net revenue.

Net revenue was $11.3 billion, an increase of $185 million, or 2%, compared with the prior year. Net interest income was $7.1 billion, down $68 million, or 1%, driven by spread compression and lower mortgage warehouse balances, predominantly offset by higher deposit balances. Noninterest revenue was $4.2 billion, an increase of $253 million, or 6%, driven by a non-recurring gain in Mortgage Banking, higher mortgage fees and related income and higher investment revenue in Consumer & Business Banking.

The provision for credit losses was $902 million, compared with a benefit of $267 million in the prior year. The current-quarter provision reflected a $200 million reduction in the allowance for loan losses and total net charge-offs of $1.1 billion. The prior-year provision reflected a $1.6 billion reduction in the allowance for loan losses and total net charge-offs of $1.3 billion.

Noninterest expense was $6.3 billion, a decrease of $562 million, or 8%, from the prior year, driven by lower Mortgage Banking expense, partially offset by an accrual related to Home Depot fraud and higher Auto lease depreciation expense.

Key Metrics and Business Updates:

(All comparisons refer to the prior-year quarter except as noted

- Return on equity was 19% on $51.0 billion of average allocated capital1.

- Average total deposits were $492.0 billion, up 8% from the prior year and 1% from the prior quarter. Ranked #1 in deposit growth for the third consecutive year1

- Record client investment assets were $207.8 billion, up 16% from the prior year and 1% from the prior quarter.

- Business Banking originations were $1.6 billion, up 27% from the prior year and down 14% from the prior quarter. Average Business Banking loans were $19.5 billion, up 5% from the prior year and 1% from the prior quarter.

- Over $600 billion, or approximately 16% of total U.S. credit and debit purchase volume1.

- Credit card sales volume1 was $119.5 billion, up 12% from the prior year. General purpose credit card sales volume growth has outperformed the industry for 26 consecutive quarters1.

- Period-end Credit Card loan balances were $127.0 billion, up $3.0 billion, or 2% from the prior year.

- Merchant processing volume was $213.3 billion, up 15% from the prior year and 2% from the prior quarter. Total transactions processed were 9.4 billion, up 6% from the prior year.

- Auto originations were $6.8 billion, up 6% from the prior year and down 4% from the prior quarter.

- Mortgage originations were $21.2 billion, down 48% from the prior year and up 26% from the prior quarter.

- Active mobile customers were up 22% over the prior year to 18.4 million, and Chase.com remains the #1 most visited banking portal in the U.S.1

Consumer & Business Banking net income was $914 million, an increase of $152 million, or 20%, compared with the prior year, predominantly due to higher net revenue.

Net revenue was $4.6 billion, up 5% compared with the prior year. Net interest income was $2.8 billion, up 4% compared with the prior year, driven by higher deposit balances, largely offset by deposit spread compression. Noninterest revenue was $1.9 billion, an increase of 6%, driven by higher investment revenue, reflecting record client investment assets, higher deposit-related fees and higher debit card revenue.

Noninterest expense was $3.0 billion, down 1% from the prior year, reflecting efficiency improvements in the business, offset by increased cost of controls.

Key Metrics and Business Updates:

(All comparisons refer to the prior-year quarter except as noted)

- Return on equity was 33% on $11.0 billion of average allocated capital.

- Ranked #1 in customer satisfaction among the largest U.S. banks for the second consecutive year, according to American Customer Satisfaction Index ("ACSI").

- Average total deposits were $476.2 billion, up 9% from the prior year and 1% from the prior quarter.

- Deposit margin was 2.20%, compared with 2.32% in the prior year and 2.23% in the prior quarter.

- Households totaled 25.6 million, up 3% from the prior year and flat compared with the prior quarter.

Mortgage Banking net income was $439 million, a decrease of $266 million from the prior year, driven by a lower benefit from the provision for credit losses, largely offset by lower noninterest expense.

Net revenue was $2.0 billion, a decrease of $36 million compared with the prior year. Net interest income was $1.0 billion, a decrease of $127 million, or 11%, driven by lower warehouse balances, spread compression and lower loan balances due to portfolio runoff. Noninterest revenue was $968 million, an increase of $91 million, driven by a non-recurring gain and higher mortgage fees and related income, partially offset by lower revenue from an exited non-core product.

The provision for credit losses was a benefit of $19 million1, compared with a benefit of $1.0 billion in the prior year. The current quarter reflected a $100 million reduction in the allowance for loan losses, reflecting continued improvement in home prices and delinquencies. The prior year included a $1.3 billion reduction in the allowance for loan losses. Net charge-offs were $81 million, compared with $206 million in the prior year.

Noninterest expense was $1.3 billion, a decrease of $621 million, or 33%, from the prior year, due to lower expense in production and servicing reflecting lower headcount.

Mortgage Production pretax income was $74 million, a decrease of $16 million from the prior year, reflecting lower revenue and lower benefit from repurchase losses, predominantly offset by lower expense. Mortgage production-related revenue, excluding repurchase losses, was $393 million, a decrease of $191 million from the prior year, primarily on lower volumes. Production expense1 was $381 million, a decrease of $288 million from the prior year, largely due to lower headcount-related expense. Repurchase losses for the current quarter reflected a benefit of $62 million, compared with a benefit of $175 million in the prior year.

Mortgage Servicing pretax income was $138 million, compared with a loss of $406 million in the prior year, reflecting lower expenses and higher MSR risk management income. Mortgage net servicing-related revenue was $639 million, an increase of $7 million from the prior year. MSR risk management income was $76 million, compared with a loss of $180 million in the prior year. Servicing expense1 was $577 million, a decrease of $281 million from the prior year due to lower expense for foreclosure-related matters and lower headcount-related expense.

Key Metrics and Business Updates:

(All comparisons refer to the prior-year quarter except as noted)

- Mortgage originations were $21.2 billion, down 48% from the prior year and up 26% from the prior quarter

- Period-end total third-party mortgage loans serviced were $766.3 billion, down 8% from the prior year and 3% from the prior quarter.

Real Estate Portfolios pretax income was $512 million, down $968 million from the prior year, driven by a lower benefit from the provision for credit losses.

Net revenue was $714 million, a decrease of $171 million from the prior year, driven by lower noninterest revenue due to higher loan retention, and lower net interest income. Net interest income was lower due to spread compression and lower loan balances due to portfolio runoff.

The provision for credit losses was a benefit of $19 million, compared with a benefit of $1.0 billion in the prior year. The current-quarter provision reflected a $100 million reduction in the non credit-impaired allowance for loan losses, reflecting continued improvement in home prices and delinquencies. The prior-year provision included a $750 million reduction in the purchased credit-impaired allowance for loan losses and $500 million reduction in the non credit-impaired allowance for loan losses. Net charge-offs were $81 million, compared with $204 million in the prior year. Home equity net charge-offs were $95 million (0.70% net charge-off rate1), compared with $218 million (1.42% net charge-off rate1)) in the prior year. Subprime mortgage net recoveries were $25 million (1.68% net recovery rate1),compared with net recoveries of $4 million (0.21% net recovery rate1). Prime mortgage, including option ARMs, net charge-offs were $9 million (0.06% net charge-off rate1), compared with net recoveries of $11 million (0.09% net recovery rate1).

Noninterest expense was $321 million, a decrease of $54 million, or 14%, compared with the prior year, driven by lower foreclosed asset expense and lower servicing expense on lower default volumes.

Key Metrics and Business Updates:

(All comparisons refer to the prior-year quarter except as noted. Average loans include PCI loans)

- Mortgage Banking return on equity was 10% on $18.0 billion of average allocated capital.

- Average home equity loans were $71.4 billion, down $9.3 billion.

- Average mortgage loans were $94.5 billion, up $4.8 billion.

- Allowance for loan losses was $5.9 billion, compared with $7.7 billion.

- Allowance for loan losses to ending loans retained, excluding PCI loans1, was 1.92%, compared with 2.39%

- Allowance for loan losses, excluding PCI loans1, to nonaccrual loans retained was 41%, compared with 40%.

Card, Merchant Services & Auto net income was $1.1 billion, a decrease of $120 million, or 10%, compared with the prior year, predominantly driven by higher provision for credit losses.

Net revenue was $4.6 billion, flat compared with the prior year. Net interest income was $3.3 billion, down $43 million compared with the prior year, driven by spread compression, partially offset by higher loan balances. Noninterest revenue was $1.4 billion, up $54 million compared with the prior year, driven by higher Auto lease income, higher net interchange income and higher annual fee income, predominantly offset by higher amortization of new account origination costs.

The provision for credit losses was $846 million, compared with $673 million in the prior year. The current-quarter provision reflected lower net charge-offs and a $100 million reduction in the allowance for loan losses in Auto and Student. The prior-year provision reflected a $351 million reduction in the allowance for loan losses in Credit Card. The Credit Card net charge-off rate was 2.52%, down from 2.86% in the prior year and the 30+ day delinquency rate was 1.43%, down from 1.69% in the prior year. The Auto net charge-off rate was 0.38%, up from 0.35% in the prior year.

Noninterest expense was $2.0 billion, up $77 million, or 4%, from the prior year, predominantly driven by an accrual related to Home Depot fraud and higher Auto lease depreciation expense.

Key Metrics and Business Updates:

(All comparisons refer to the prior-year quarter except as noted)

- Return on equity was 23% on $19.0 billion of average allocated capital.

- #1 credit card issuer in the U.S. based on loans outstanding1.

- #1 U.S. co-brand credit card issuer1.

- #1 global Visa issuer1.

- Period-end Credit Card loan balances were $127.0 billion, up 2% from the prior year and 1% from the prior quarter. Credit Card average loans were $126.1 billion, up 2% from the prior year and prior quarter.

- Card Services net revenue as a percentage of average loans was 12.07%, compared with 12.22% in the prior year and 12.15% in the prior quarter.

- Average auto loans were $52.7 billion, up 4% from the prior year and flat compared with the prior quarter.

- #1 wholly-owned merchant acquirer with approximately 50% of U.S. eCommerce volume1.

CORPORATE & INVESTMENT BANK (CIB)

| Results for CIB ($ millions) | 3Q14 | 2Q14 | 3Q13 | 2Q14 | 3Q13 |

|---|

| $ O/(U) | O/(U) % | $ O/(U) | O/(U) % |

|---|

| Net Revenue | $ 8,787 | $ 8,991 | $ 8,189 | $ (204) | (2)% | $ 598 | 7% |

| Provision for Credit Losses | (67) | (84) | (218) | 17 | (20) | 151 | (69) |

| Noninterest Expenses | 6,035 | 6,058 | 4,999 | (23) | - | 1036 | 21 |

| Net Income | $ 1,485 | $ 1,963 | $ 2,240 | $ (478) | (24%) | (755) | (34)% |

Discussion of Results:

Net income was $1.5 billion, down 34%, compared with $2.2 billion in the prior year reflecting higher noninterest expense and a lower benefit from the provision for credit losses, largely offset by higher net revenue. Net revenue was $8.8 billion compared with $8.2 billion in the prior year. Excluding the impact of a DVA loss of $397 million in the prior year, net revenue was up 2% from $8.6 billion and net income was down 40% from $2.5 billion.

Banking revenue was $2.7 billion, down 6% from the prior year. Investment banking fees were $1.5 billion, up 2% from the prior year, driven by higher advisory fees of $413 million, up 28% from the prior year, and by higher equity underwriting fees of $414 million, up 24% from the prior year, on higher levels of industry-wide activity. These increases were predominantly offset by lower debt underwriting fees of $715 million, down 16% from a strong prior year. Treasury Services revenue was $1.0 billion, down 2% compared with the prior year, driven by lower trade finance revenue and the impact of business simplification initiatives, predominantly offset by higher net interest income on increased deposits. Lending revenue was $147 million, down from $351 million in the prior year, primarily driven by losses of over $100 million on securities received from restructured loans, compared to modest gains in the prior period.

Markets & Investor Services revenue was $6.1 billion, up 15% from the prior year. Fixed Income Markets revenue of $3.5 billion was up 2% from the prior year with particularly strong performance in currencies and emerging markets. Equity Markets revenue of $1.2 billion was down 1% compared with the prior year, primarily on lower derivatives revenue compared to a strong prior year largely offset by higher prime services revenue. Securities Services revenue was $1.1 billion, up 8% from the prior year primarily driven by higher net interest income on increased deposits and higher fees and commissions. Credit Adjustments & Other revenue was a gain of $240 million, primarily driven by DVA/FVA as a result of credit spread widening and refinements to certain funding assumptions, compared with a loss of $409 million in the prior year which was primarily driven by DVA.

TThe provision for credit losses was a benefit of $67 million, compared with a benefit of $218 million in the prior year. The ratio of the allowance for loan losses to period-end loans retained was 1.13%, compared with 1.09% in the prior year. Excluding the impact of the consolidation of Firm-administered multi-seller conduits and trade finance loans, the ratio of the allowance for loan losses to period-end loans retained1 was 1.88%, compared with 2.01% in the prior year.

Noninterest expense was $6.0 billion, up 21% from the prior year, driven by higher legal expense and higher compensation expense. The ratio of compensation expense to total net revenue was 32%.

Key Metrics and Business Updates:

(All comparisons refer to the prior-year quarter except as noted, and all rankings are according to Dealogic)

- Return on equity was 10% on $61.0 billion of average allocated capital.

- Overhead ratio was 69%.

- Ranked #1 in Global Investment Banking fees with 8.0% wallet share for the nine months ended September 30, 2014.

- Ranked #1 in Global Debt, Equity and Equity-related with 7.5% wallet share; #1 in Global Long-Term Debt with 7.7% wallet share; #1 in Global Syndicated Loans with 9.5% wallet share; #3 in Global Equity and Equity-related with 7.2% wallet share; and #2 in Global M&A, with 8.1% wallet share, based on revenue, for the nine months ended September 30, 2014.

- Average client deposits and other third-party liabilities were $419.6 billion, up 9% from the prior year and up 4% from the prior quarter.

- Assets under custody were $21.2 trillion, up 8% from the prior year and down 2% from the prior quarter.

- International revenue represented 51% of total revenue.

- Period-end total loans were $102.3 billion, down 5% from the prior year and down 6% from the prior quarter; both declines were driven by a reduction in client overdrafts.

- Nonaccrual loans were $231 million, down 40% from the prior year and down 17% from the prior quarter.

COMMERCIAL BANKING (CB)

| Results for CB ($ millions) | 3Q14 | 2Q14 | 3Q13 | 2Q14 | 3Q13 |

|---|

| $ O/(U) | O/(U) % | $ O/(U) | O/(U) % |

|---|

| Net Revenue | $ 1,667 | $ 1,701 | $ 1,725 | $ (34) | (2)% | $ (58) | (3)% |

| Provision for Credit Losses | (79) | (67) | (41) | (12) | 18 | (38) | 93 |

| Noninterest Expenses | 668 | 675 | 661 | (7) | (1) | 7 | 1 |

| Net Income | $ 649 | $ 658 | $ 665 | $ (9) | (1)% | $ (16) | (2)% |

Discussion of Results:

Net income was $649 million, a decrease of $16 million, or 2%, compared with the prior year, reflecting lower net revenue, largely offset by a lower provision for credit losses.

Net revenue was $1.7 billion, a decrease of $58 million, or 3%, compared with the prior year. Net interest income was $1.1 billion, a decrease of $41 million, or 4%, compared with the prior year, reflecting yield compression and lower purchase discounts recognized on loan repayments, largely offset by higher loan balances. Noninterest revenue was $571 million, a decrease of $17 million, or 3%, compared with the prior year, driven by business simplification and lower other fees, partially offset by higher investment banking revenue.

Revenue from Middle Market Banking was $684 million, a decrease of $61 million, or 8%, compared with the prior year. Revenue from Corporate Client Banking was $480 million, an increase of $21 million, or 5%, compared with the prior year. Revenue from Commercial Term Lending was $303 million, a decrease of $8 million, or 3%, compared with the prior year. Revenue from Real Estate Banking was $121 million, an increase of $3 million, or 3%, compared with the prior year.

The provision for credit losses was a benefit of $79 million, compared with a benefit of $41 million in the prior year. Net charge-offs were $5 million (0.01% net charge-off rate), compared with net charge-offs of $16 million (0.05% net charge-off rate) in the prior year and net recoveries of $26 million (0.07% net recovery rate) in the prior quarter. The allowance for loan losses to period-end loans retained was 1.76%, down from 1.99% in the prior year and down from 1.87% in the prior quarter. Nonaccrual loans were $375 million, down $191 million, or 34%, from the prior year, and down $71 million, or 16%, from the prior quarter.

Noninterest expense was $668 million, flat compared with the prior year.

Key Metrics and Business Updates:

(All comparisons refer to the prior-year quarter except as noted)

- Return on equity was 18% on $14.0 billion of average allocated capital.

- Overhead ratio was 40%, compared with 38% in the prior year.

- Gross investment banking revenue (which is shared with the Corporate & Investment Bank) was $501 million, up 12% compared with the prior year and 4% compared with the prior quarter. Record YTD gross investment banking revenue of $1.4 billion, up 22% from the prior year.

- Average loan balances were $142.8 billion, up 8% compared with the prior year and 1% compared with the prior quarter.

- Period-end loan balances were $143.8 billion, up 6% compared with the prior year and 1% compared with the prior quarter.

- Average client deposits and other third-party liabilities were $204.7 billion, up 4% compared with the prior year and 2% compared with the prior quarter.

ASSET MANAGEMENT (AM)

| Results for AM ($ millions) | 3Q14 | 2Q14 | 3Q13 | 2Q14 | 3Q13 |

|---|

| $ O/(U) | O/(U) % | $ O/(U) | O/(U) % |

|---|

| Net Revenue | $ 3,016 | $ 2,956 | $ 2,763 | $ 60 | 2% | 253$ - | 9% |

| Provision for Credit Losses | 9 | 1 | - | 8 | NM | 9 | NM |

| Noninterest Expenses | 2,081 | 2,062 | 2,003 | 19 | 1 | 78 | 4 |

| Net Income | $ 572 | $ 552 | $ 476 | $ 20 | 4% | $ 96 | 20% |

Discussion of Results:

Net income was $572 million, an increase of $96 million, or 20%, from the prior year, reflecting higher net revenue, partially offset by higher noninterest expense.

Net revenue was $3.0 billion, an increase of $253 million, or 9%, from the prior year. Noninterest revenue was $2.4 billion, up $237 million, or 11%, from the prior year, due to net client inflows and the effect of higher market levels. Net interest income was $594 million, up $16 million, or 3%, from the prior year, due to higher loan and deposit balances, partially offset by spread compression.

Revenue from Global Investment Management was $1.6 billion, up 13% compared with the prior year. Revenue from Global Wealth Management was $1.4 billion, up 5%.

Client assets were $2.3 trillion, an increase of $98 billion, or 4%, compared with the prior year. Excluding the sale of Retirement Plan Services, client assets were up 10% compared with the prior year. Assets under management were $1.7 trillion, an increase of $171 billion, or 11%, from the prior year, due to the effect of higher market levels and net inflows to long-term products.

The provision for credit losses was $9 million, compared with a negligible provision for credit losses in the prior year.

Noninterest expense was $2.1 billion, an increase of $78 million, or 4%, from the prior year, as the business continues to invest in both infrastructure and controls.

Key Metrics and Business Updates:

(All comparisons refer to the prior-year quarter except as noted)

- Return on equity was 25% on $9.0 billion of average allocated capital.

- Pretax margin1 was 31%, up from 28% in the prior year.

- For the 12 months ended September 30, 2014, assets under management reflected net inflows of $84 billion, predominantly driven by long-term products. For the quarter, net inflows were $24 billion, driven by net inflows of $16 billion to long-term products and $8 billion to liquidity products.

- Net long-term client flows were positive for the twenty-second consecutive quarter.

- Assets under management ranked in the top two quartiles for investment performance were 71% over 5 years, 69% over 3 years and 54% over 1 year.

- Customer assets in 4 and 5 Star-rated funds were 49% of all rated mutual fund assets.

- Client assets were $2.3 trillion, up 4% from the prior year and down 5% from the prior quarter.

- Average loans were $101.4 billion, a record, up 16% from the prior year and 3% from the prior quarter.

- Average deposits were $151.2 billion, a record, up 9% from the prior year and 2% from the prior quarter.

CORPORATE/PRIVATE EQUITY

| Results for Corporate/Private Equity ($ millions) | 3Q14 | 2Q14 | 3Q13 | 2Q14 | 3Q13 |

|---|

| $ O/(U) | O/(U) % | $ O/(U) | O/(U) % |

|---|

| Net Revenue | $ 422 | $ 270 | $ 121 | $ 152 | 56% | $ 301 | 249% |

| Provision for Credit Losses | (8) | (10) | (17) | 2 | 20 | 9 | 53 |

| Noninterest Expenses | 709 | 180 | 9,096 | 529 | 294 | (8,387) | (92)% |

| Net Income | $ 398 | $ 369 | $ (6,463) | $ 29 | 8% | $ 6,861 | NM |

Discussion of Results:

Net income was $398 million, compared with a net loss of $6.5 billion in the prior year.

Private Equity reported net income of $71 million, compared with net income of $242 million in the prior year, primarily due to lower net valuation gains on investments.

Treasury and CIO reported a net loss of $30 million, compared with a net loss of $193 million in the prior year. Net revenue was $132 million, compared with a loss of $232 million in the prior year. Net interest income was a gain of $36 million, compared with a loss of $261 million in the prior year, primarily reflecting the benefit of higher re-investment yields and higher investment securities balances.

Other Corporate reported net income of $357 million, compared with a net loss of $6.5 billion in the prior year. The current quarter included $512 million (pretax) of legal expense, compared with approximately $9.2 billion (pretax) of legal expense in the prior year. The current quarter also included approximately $400 million of net income benefit from tax adjustments.

JPMORGAN CHASE (JPM)(*)

| Results for JPM ($ millions) | 3Q14 | 2Q14 | 3Q13 | 2Q14 | 3Q13 |

|---|

| $ O/(U) | O/(U) % | $ O/(U) | O/(U) % |

|---|

| Net Revenue | $ 25,159 | $ 25,349 | $ 23,880 | $ (190) | (1)% | $ 1,279 | 5% |

| Provision for Credit Losses | 757 | 692 | (543) | 65 | 9% | 1300 | NM |

| Noninterest Expenses | 15,798 | 15,431 | 23,626 | 367 | 2 | (7,828) | (33) |

| Net Income | $ 5,572 | $ 5,985 | $ (380) | $ 413 | (7)% | $ 5,952 | NM |

(*)Presented on a managed basis. See note on page 12 for further explanation of managed basis. Net revenue on a U.S. GAAP basis totaled $22.5 billion, $24.2 billion, and $23.2 billion for the fourth quarter of 2014, third quarter of 2014, and fourth quarter of 2013, respectively.

Discussion of Results:

Net income was $5.6 billion, compared with a loss of $380 million in the prior year. The increase was driven by lower noninterest expense and higher net revenue, partially offset by higher provision for credit losses.

Net revenue was $25.2 billion, up $1.3 billion, or 5%, compared with the prior year. Noninterest revenue was $13.8 billion, up $875 million, or 7%, compared with the prior year. Net interest income was $11.4 billion, up $404 million, or 4%, compared with the prior year, reflecting lower interest expense and higher investment securities yields, partially offset by lower loan yields.

The provision for credit losses was an expense of $757 million, compared with a benefit of $543 million in the prior year. The total consumer provision for credit losses was an expense of $897 million, compared with a benefit of $273 million in the prior year. The current-quarter consumer provision reflected a $200 million reduction in the allowance for loan losses, compared to a $1.6 billion reduction in the prior year. The current-quarter consumer allowance release primarily reflects the continued improvement in home prices and delinquency trends in the residential real estate portfolio and the run-off of the student loan portfolio. Consumer net charge-offs were $1.1 billion, compared with $1.3 billion in the prior year, resulting in net charge-off rates of 1.19% and 1.47%, respectively.

The wholesale provision for credit losses was a benefit of $140 million, compared with a benefit of $270 million in the prior year. Wholesale net charge-offs were $17 million, compared with $26 million in the prior year, resulting in net charge-rates of 0.02% and 0.03%, respectively.

The Firm's allowance for loan losses to period-end loans retained1 was 1.63%, compared with 1.89% in the prior year. The Firm's allowance for loan losses to nonperforming loans retained1 was 155%, compared with 140% in the prior year. The Firm's nonperforming assets totaled $8.4 billion, down from the prior quarter and prior year levels of $9.0 billion and $10.4 billion, respectively.

Noninterest expense was $15.8 billion, down $7.8 billion, or 33%, compared with the prior year, driven by lower legal expense. The current quarter noninterest expense included approximately $1.1 billion of legal expense, compared with approximately $9.3 billion of legal expense in the prior year.

1. Notes on non-GAAP financial measures:

- In addition to analyzing the Firm's results on a reported basis, management reviews the Firm's consolidated results and the results of the lines of business on a "managed" basis, which is a non-GAAP financial measure. The Firm's definition of managed basis starts with the reported U.S. GAAP results and includes certain reclassifications to present total consolidated net revenue for the Firm (and for each of the business segments) on a fully taxable-equivalent ("FTE") basis. Accordingly, revenue from investments that receive tax credits and tax-exempt securities is presented in the managed results on a basis comparable to taxable securities and investments. This non-GAAP financial measure allows management to assess the comparability of revenue arising from both taxable and tax-exempt sources. The corresponding income tax impact related to tax-exempt items is recorded within income tax expense. These adjustments have no impact on consolidated net income/(loss) as reported by the Firm or on net income/(loss) as reported by the lines of business.

- The ratio of the allowance for loan losses to end-of-period loans retained, and the allowance for loan losses to nonaccrual loans retained, exclude the following: loans accounted for at fair value and loans held-for-sale; purchased credit-impaired ("PCI") loans; and the allowance for loan losses related to PCI loans. Additionally, net charge-offs and net charge-off rates exclude the impact of PCI loans.

- Tangible common equity ("TCE") and return on tangible common equity ("ROTCE") are each non-GAAP financial measures. TCE represents the Firm's common stockholders' equity (i.e., total stockholders' equity less preferred stock) less goodwill and identifiable intangible assets (other than MSRs), net of related deferred tax liabilities. ROTCE measures the Firm's earnings as a percentage of average TCE. TCE and ROTCE are meaningful to management, as well as analysts and investors, in assessing the Firm's use of equity, as well as facilitating comparisons of the Firm with competitors.

- Common Equity Tier 1 ("CET1") capital and the CET1 ratio under the Basel III Advanced Fully Phased-In rules, and the supplementary leverage ratio ("SLR") under the U.S. final SLR rule, are each non-GAAP financial measures. These measures are used by management, bank regulators, investors and analysts to assess and monitor the Firm's capital position. For additional information on these measures, see Regulatory capital on pages 161-165 of JPMorgan Chase & Co.'s Annual Report on Form 10-K for the year ended December 31, 2013, and on pages 73-77 of the Firm's Quarterly Report on Form 10-Q for the quarter ended September 30, 2014.

- The CIB provides non-GAAP financial measures, as such measures are used by management to assess the underlying performance of the business and for comparability with peers.

- The ratio of the allowance for loan losses to end-of-period loans excludes the impact of consolidated Firm-administered multi-seller conduits and trade finance loans, to provide a more meaningful assessment of CIB's allowance coverage ratio.

- ROE for the fourth quarter 2014 is calculated excluding legal expense.

- Prior to January 1, 2014, the CIB provided non-GAAP financial measures excluding the impact of FVA (effective fourth quarter 2013) and DVA on net revenue and net income. Beginning in the first quarter 2014, the Firm does not exclude FVA and DVA from its assessment of business performance, with the exception of certain refinements to net FVA and DVA in the fourth quarter 2014; however, the Firm continues to present these non-GAAP measures for the periods prior to January 1, 2014, as they reflected how management assessed the underlying business performance of the CIB in those prior periods.

- The change in Fixed Income Markets revenue excludes the revenue decline related to business simplification, including the sales of Physical Commodities and Global Special Opportunities Group businesses.

2. Additional notes on financial measures:

- Core loans include loans considered central to the Firm's ongoing businesses; core loans exclude runoff portfolios, discontinued portfolios and portfolios the Firm has an intent to exit.

- The amount of credit provided to clients represents new and renewed credit, including loans and commitments. The amount of credit provided to small businesses reflects loans and increased lines of credit provided by Consumer & Business Banking; Card, Merchant Services & Auto; and Commercial Banking. The amount of credit provided to nonprofit and government entities, including states, municipalities, hospitals and universities, represents that provided by the Corporate & Investment Bank and Commercial Banking.

- Consumer & Community Banking 2014 allocated equity includes $3.0 billion of capital held at the Consumer & Community Banking level related to legacy mortgage servicing matters.

- Consumer & Business Banking deposit rankings are based on FDIC 2014 Summary of Deposits survey per SNL Financial.

- The credit and debit volume metric is based on Nilson data as of 2013.

- Credit card sales volume is presented excluding Commercial Card. Rankings and comparison of general purpose credit card sales volume are based on disclosures by peers and internal estimates. Rankings are as of 3Q14.

- Banking portal ranking is per compete.com, as of November 2014.

- Mortgage Banking provision for credit losses is included in Real Estate Portfolios, in production expense in Mortgage Production, and in core servicing expense in Mortgage Servicing.

- #1 credit card issuer and 21% market share rankings based on disclosures by peers and internal estimates as of 3Q14.

- #1 U.S. co-brand issuer based on Phoenix Credit Card Monitor for the 12-months period ending September 2014; based on card accounts and revolving balance dollars.

- Global Visa ranking based on Visa data as of 3Q14 based on consumer and business credit card sales volume.

- #1 wholly-owned merchant acquirer based on Nilson data as of 2013; share of U.S. eCommerce volume based on the Internet Retailer Top 500 for 2013 and JPMC internal merchant client data.

JPMorgan Chase & Co. (NYSE: JPM) is a leading global financial services firm and one of the largest banking institutions in the United States of America (U.S.), with operations worldwide; the Firm has $2.5 trillion in assets and $219.7 billion in stockholders' equity. The Firm is a leader in investment banking, financial services for consumers and small businesses, commercial banking, financial transaction processing, asset management and private equity. A component of the Dow Jones Industrial Average, JPMorgan Chase & Co. serves millions of consumers in the U.S. and many of the world's most prominent corporate, institutional and government clients under its J.P. Morgan and Chase brands. Information about J.P. Morgan's capabilities can be found at jpmorgan.com and about Chase's capabilities at chase.com. Information about the Firm is available at www.jpmorganchase.com.

JPMorgan Chase & Co. will host a conference call today at 8:30 a.m. (Eastern Time) to present second quarter financial results. The general public can access the call by dialing (866) 541-2724 or (866) 786-8836 in the U.S. and Canada, or (706) 634-7246 for international participants. Please dial in 10 minutes prior to the start of the call. The live audio webcast and presentation slides will be available on the Firm's website, www.jpmorganchase.com, under Investor Relations, Investor Presentations.

A replay of the conference call will be available beginning at approximately noon on July 15, 2014, through midnight, August 2, 2014, by telephone at (855) 859-2056 or (800) 585-8367 (U.S. and Canada) or (404) 537-3406 (international); use Conference ID# 51815263. The replay will also be available via webcast on www.jpmorganchase.com under Investor Relations, Investor Presentations. Additional detailed financial, statistical and business-related information is included in a financial supplement. The earnings release and the financial supplement are available at www.jpmorganchase.com.

This earnings release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are based on the current beliefs and expectations of JPMorgan Chase & Co.'s management and are subject to significant risks and uncertainties. Actual results may differ from those set forth in the forward-looking statements. Factors that could cause JPMorgan Chase & Co.'s actual results to differ materially from those described in the forward-looking statements can be found in JPMorgan Chase & Co.'s Annual Report on Form 10-K for the year ended December 31, 2013, and Quarterly Report on Form 10-Q for the quarter ended March 31, 2014, which have been filed with the Securities and Exchange Commission and are available on JPMorgan Chase & Co.'s website (https://jpmorganchaseco.gcs-web.com/financial-information/sec-filings) and on the Securities and Exchange Commission's website (www.sec.gov). JPMorgan Chase & Co. does not undertake to update the forward-looking statements to reflect the impact of circumstances or events that may arise after the date of the forward-looking statements.