Small businesses are one of the pillars of urban economies, making substantial contributions to economic growth and dynamism. However, the fragility of the small business sector is an ongoing challenge that limits how much it contributes to economic growth in cities. Nine out of ten cities in the United States are losing businesses faster than they are creating them.1 Understanding the drivers of growth and failure in the small business sector—and the variation of these drivers across cities—is critical to the development of policies that promote small business survival and growth.

This report leverages high-frequency, de-identified financial data from a sample of 290,000 small operating businesses to identify differences and similarities in small business financial outcomes across 25 US cities. A follow-up from the JPMorgan Chase Institute 2018 report on small business growth, vitality, and cash flows, this report provides a lens into the composition and contributions of different types of firms to aggregate revenue growth and exit rates of the small business sector.

Our findings are four-fold:

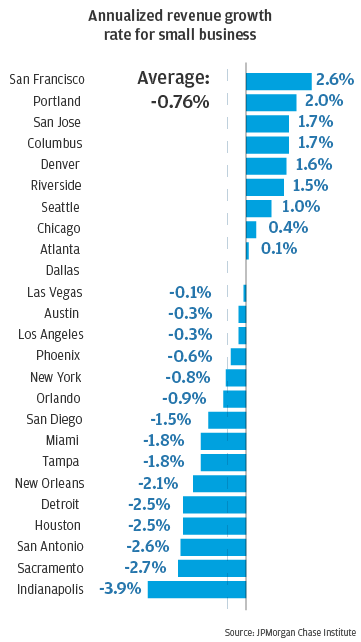

Finding 1: New firms account for most of the revenue growth in the small business sector, but their contributions to growth vary widely by city.

Finding 2: Among new small businesses, five percent of firms account for nearly all aggregate revenue growth across cities, and these usually grow organically.

Finding 3: While revenue growth rates vary substantially by industry across cities, small firms in construction, other professional services, health care services and high-tech services drive aggregate growth in most cities.

Finding 4: Across cities, retail and other professional services drive small business exits.

These findings suggest that both local and national policymakers interested in the financial health of the small business sector might benefit from paying closer attention to themes that are similar across cities, and important differences between cities. Across cities, a relatively small share of businesses drove aggregate revenue growth, but most of these firms grew without substantial reliance on external finance, and most of these firms were outside of industries typically thought of as high-growth. Moreover, while some cities maintained uniquely low small business exit rates given their revenue growth, these differences were driven more by within-industry differences in exit rates than by industry composition.