We no longer support this browser. Using a supported browser will provide a better experience.

Please update your browser.

City and regional governments spend considerable time promoting their cities to international markets whether for exports of goods or as a tourist destination. Overlooked is the importance of domestic visitors—business travelers, tourists, or day-trippers—who allow a metro area to extend its economic reach. Much as exports enable firms to reach new markets and consumers beyond their immediate surroundings, increasing the number of visitors to a metro area increases the number of potential customers. Visitors are important beyond the traditional tourist-centric sectors such as hotels or restaurants, with purchases extending into retail and entertainment amongst others. Leveraging data from 12.4 billion anonymized credit and debit card transactions in 15 metropolitan areas, the JPMorgan Chase Institute's recently released Profiles of Local Consumer Commerce (PLCC) can help better explain spending by domestic visitors in metropolitan areas.

Across the fifteen metro areas, the average share of spending by nonresidents was 15.6 percent of total consumer spending. The average masks considerable variance across the cities, as shown in the table below. In Phoenix, nonresidents accounted for 23.0 percent of all local consumer commerce spending. This is nearly 17 percentage points higher than the city with the lowest share of spending by nonresidents, Houston, where visitors only accounted for 6.1 percent of spending. Besides Phoenix, other cities at the top of the rankings include San Diego and Seattle.

| Which metro area has the largest share of spending by visitors? | ||

|---|---|---|

| Rank | Metro Area | Share of Spending |

| 1 | Phoenix-Mesa-Scottsdale, AZ | 23.0% |

| 2 | San Diego-Carlsbad, CA | 21.6% |

| 3 | Seattle-Tacoma-Bellevue, WA | 21.2% |

| 4 | San Francisco-Oakland-Hayward, CA | 20.5% |

| 5 | Atlanta-Sandy Springs-Roswell, GA | 18.3% |

| 6 | Dallas-Fort Worth-Arlington, TX | 18.1% |

| 7 | Los Angeles-Long Beach-Anaheim, CA | 17.4% |

| 8 | Portland-Vancouver-Hillsboro, OR-WA | 17.0% |

| 9 | Denver-Aurora-Lakewood, CO | 15.8% |

| – | Fifteen City Average | 15.6% |

| 10 | Miami-Fort Lauderdale-West Palm Beach, FL | 15.6% |

| 11 | Columbus, OH | 11.3% |

| 12 | Detroit-Warren-Dearborn, MI | 10.0% |

| 13 | New York-Newark-Jersey City, NY-NJ-PA | 9.8% |

| 14 | Chicago-Naperville-Elgin, IL-IN-WI | 8.3% |

| 15 | Houston-The Woodlands-Sugar Land, TX | 6.1% |

Source: JPMorgan Chase Institute.

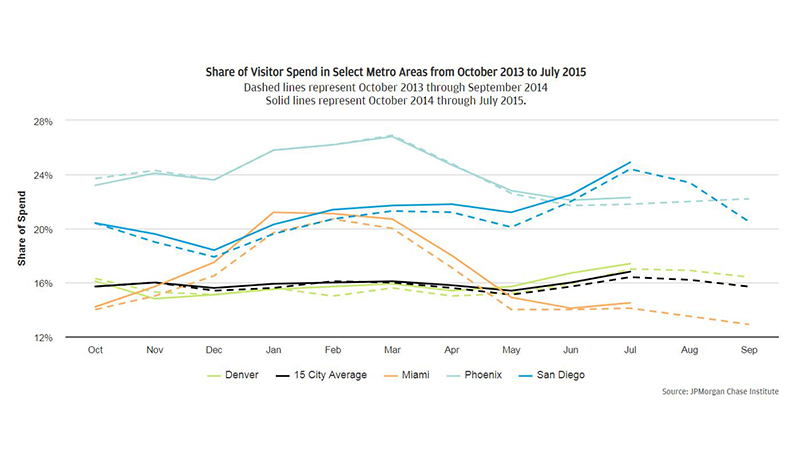

Tourism is generally considered to be highly seasonal, with many destinations known for having peak and quiet periods. However, spending by out-of-towners across most cities remains stable throughout the year, as reflected in the fifteen city average.1 Despite this relative stability, two distinct seasonality patterns emerge: (1) across several cities, notably San Diego and Denver, a slight increase in summer months; and (2) for two of the fifteen cities, Phoenix and Miami, a spike in winter months, reflecting the well-known migration to warm weather and so-called "snowbirds." Interestingly, though the pattern is similar for both cities, the level share in Phoenix is considerably higher than that in Miami—in some months higher by 10 percentage points. In the chart below, we show these patterns by plotting the share of spending by visitors in select metro areas between October 2013 and July 2015.

Visitors are only one part of local economies, but in most cities they represent a meaningful percent of local consumer commerce and thus can be an important market for firms looking to expand beyond the immediate residents of their metro area. The JPMorgan Chase Institute's new data series, Profiles of Local Consumer Commerce, enables better tracking of these data within and across metropolitan areas, and is a powerful tool for understanding consumer commerce and devising better policies to enable commerce.

The JPMorgan Chase Institute is committed to delivering data-rich analyses and expert insights for the public good. Our recently released report Profiles of Local Consumer Commerce tells the story of the decline in everyday retail spending across fifteen metro areas. Over the next five weeks, the JPMC Institute will explore the differences between the metro areas through a series of blog posts ranking the cities across select dimensions from the report.

JPMorgan Chase & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. Please review its website terms, privacy and security policies to see how they apply to you. JPMorgan Chase & Co. isn't responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the JPMorgan Chase & Co.